Stick It!

Although we featured pithy weekly commentaries in this space for many years, the time and effort spent crafting them is now devoted to making the Rick’s Picks Trading Room an unbeatable source of timely trading ideas for novices and professionals. You should check here weekly, since I will continue to post links to my latest interviews and to offer visual enticements designed to entertain, amuse and enlighten you. Much of it will come from YouTube, since their video catalog is endlessly fascinating. Submissions, including home videos, are welcome and should be sent to this address. To get things rolling, click here for an unbelievable drum solo that demonstrates why the late Buddy Rich would never have worried about being replaced by a synthesizer. The headline is the title of one of his many albums.

Subscribe Free!

The analytical ‘touts’ below, overhauled each Sunday and updated 24/7, will continue as always, as will their barbed emphasis on the similarities between Wall Street and sleazy carnival midways. The remarkable accuracy of our trend calls and price targets is a matter of daily record and must be observed up close to be believed. Sign up for a free trial with access to all site amenities by clicking here (no credit card needed). Then click here for my most recent interview with Howe Street’s Jim Goddard. We talk about the Information Age and whether there is enough value in manipulating data to keep America prosperous and to support grotesquely bloated asset prices.

Still Fishin’…

I’m taking an extended break from the daunting challenge of predicting the stock market’s behavior each week as though it were correlated rationally and logically with events in the real world. My weekly commentaries will resume when I am feeling better up to the task. In the meantime, if you need a regular dose of Rick’s Picks, don’t pass up a free opportunity to use and enjoy all of the site’s amenities, including the Trading Room, the heart and soul of my service. Its purpose is to help investors make money, a goal it achieves so consistently that gifted traders from around the world like to hang out there. The photo above shows Venezuela’s Angel Falls, the world’s highest waterfall and a good metaphor for my outlook on the stock market. Finally, here’s a link to my latest rant at This Week in Money on July 2. [Note: This link will change to present fresh material every other week.]

Into Thin Air

These weekly commentaries have struggled to make sense of a world in geopolitical chaos but which is nonetheless transfixed by a financial melt-up that cannot end other than disastrously. Still more challenging is predicting the day-to-day effects on a stock market whose behavior is a perfect analog for acute, mass mental illness. By ascending without pause into celestial heights, the market is saying it doesn’t give a fuck about the Strait of Hormuz, war with Iran, the AI bubble, Trump’s falling poll numbers, Europe’s decline into economic darkness, rising oil prices that threaten to implode the global economy, bloated earnings multiples, stubbornly firm interest rates, a big victory for Democrats in November, or a next round of inflation that will make what has occurred so far seem like just a warm-up.

Bloomberg’s Dart Board

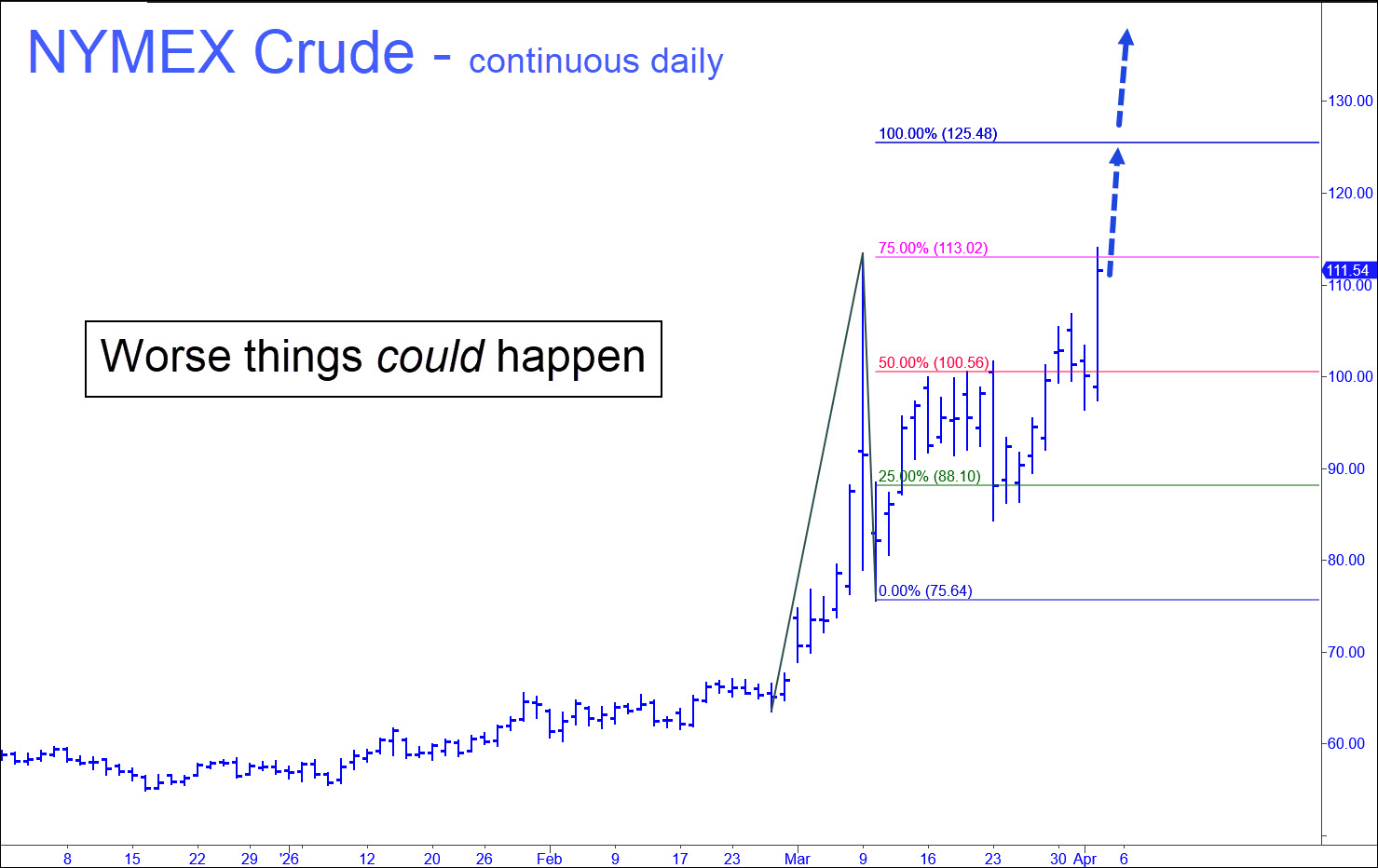

Concerning the price of crude oil, let me cut to the chase so that you don’t have to waste precious time listening to some amateur on Bloomberg choke out dart-board guesses: NYMEX June Crude, which settled on Friday at 102.50, down 2.57 a barrel, is about to rise to 128.19. Furthermore, if it relapses to 91.28 in the interim, don’t mistake this for a sign of respite; for in fact, crude would become a fetching “buy” there, predicated on an implied 40% run-up to 128.19. While that might be enough to wipe the idiotic grin from Wall Street’s face, don’t be surprised if the broad averages seem to hold their own. Whatever it takes to end the 17-year-old bull market is probably too terrifying to imagine. But the catalyst will necessarily be deflationary, since the bull market has been built on an expansionary mindset that has multiplied and rotated OPM into stocks that have faced little resistance. Insiders have finally begun to sell, and so should you.

Craving a Token Piece of the Rock?

Is there a tokenized investment in your future? With so many white elephants to unload, Wall Street’s rep could come calling on you at any time. He will offer you a virtual piece of America’s future, claiming it will grow wealth for your children and grandchildren. However, when you sit down with this cheery fellow to go over the fine print, just remember that his brain is nearly identical genetically to that of the seagull that swoops down on your lunch at a seaside café.

Is there a tokenized investment in your future? With so many white elephants to unload, Wall Street’s rep could come calling on you at any time. He will offer you a virtual piece of America’s future, claiming it will grow wealth for your children and grandchildren. However, when you sit down with this cheery fellow to go over the fine print, just remember that his brain is nearly identical genetically to that of the seagull that swoops down on your lunch at a seaside café.

And exactly which piece of the rock will your hard-earned dollars secure? Almost certainly, the pitch will feature commercial real estate or AI infrastructure. The latter will include not only huge power plants and water coolers, along with acres of computers, but all the hot air exhausted by a Billionaire Boy’s Club that has been hustling some of the most ambitious projects the galaxy has ever seen.

Hot Air for Sale

Obsolete skyscrapers and AI’s overhyped revenue potential are the chief sources of anxiety in banksters’ portfolios these days, with notional sums at risk of perhaps $20 trillion or more, and growing. All of it has been financed to colossal excess by banks that have grown understandably eager to spread the risk onto rubes like you and me. Voila, the tokenized investment! That’s why tokens were invented: to divvy up epic chunks of glitz into a million pieces small enough for the little guy to get in on the action.

He needn’t worry about being shut out, since the deals just keep coming. So greedy and stupid are the lenders that they are still hatching galactically large projects even as warning signs flash red. Oracle’s partnership with OpenAI, for instance. This gambit is slated to launch in 2027 at a value of $500 billion. The two companies would build data centers with 4.5 gigawatts of capacity, a tad less than New York City’s annual usage. Will the demand be there? Everyone on the sell side of the equation sems to think so, but the view is not so optimistic among highly paid tech workers whose jobs are becoming obsolete these days by the tens of thousands.

Skyscrapers Are Dead

Real estate will be a tougher sell for Wall Street’s seagull-brained predators, since all of us understand that workers will never return to urban office towers. Their employers cannot successfully order them back, either, since, for reasons of cost and competitive pressures, most big companies no longer do business out of center-city skyscrapers. Still, there the buildings sit, urgently in need of hucksters to spread the cost of perpetually financing and maintaining them over however many Millennials and Gen-Xers are fortunate enough to have savings to invest.

Thus, tokenized investments. It’s curious that this meme is being plumped for such an ambitious pitch, since we commonly associate the word ‘token’ with things that have no substance. As such, you could say that the sales force about to hit the streets with tokenized shares of office towers and AI infrastructure is like a belled cat, well exposed before they knock on your door. When they arrive, keep the latch on and make them explain, exactly, what they are selling. (More on the coming AI job bust: Check out my latest interview with Jim Goddard on This Week in Money.)

Explosive Rally Is a Dangerous Deception

You can hardly blame Trump for playing up the stock market’s spectacular performance whenever anyone challenges the way he is conducting the war, or claims the jihadists are winning. Even in the editorial rooms of the New York Times and Bloomberg, where a virulent strain of Trump Derangement Syndrome still lingers, news editors are finding their caustic opinions overwhelmed by the bullish tide — make that, tsunami — on Wall Street. Although details of a cease-fire have yet to be worked out, never mind the terms of a peace agreement, stocks have exploded into their steepest rally ever, recouping five months’ worth of steady losses in just 17 days, while racking up gains during that period equal to the amazing, six-month bull run-up of 2025. Can tens of millions of investors be wrong? Or is genuine peace about to break out, as Trump would put it, like nothing the world has ever seen before?

To answer that question, harken back to an iconic graffito from the 1970s: “Eat Shit! Can a hundred trillion flies be wrong?” If you fail to see the connection, let me spell it out: A superheated stock market is the last place everyone should look for evidence that all is right with the world. Moreover, Trump’s eagerness to direct our attention that way makes it even more foolhardy.

Bipolarity’s Sweet Spot

Why? Because the stock market is a rabid beast whose mood swings have always ranged between reckless exuberance and suicidal despair. Within the broad middle of this bipolarity, it acts like a giant carnival midway, hyped by barkers who use ‘research’ to support extremes of overvaluation that currently make the South Sea Bubble of the 1700s look like a shingles-and-siding hustle.

Moreover, the rally’s aberrant strength suggests it is driven mainly by a short-covering panic rather than by bullish buying. Or should we infer instead that investors actually believe world peace is about to break out, or that oil prices will quickly fall back to bargain levels following the most severe shock that energy markets have experienced since prices quadrupled in the early 1970s?

Deflationary ‘Cure’

As stocks soar into new record territory, serious doubts grow that the U.S. and global economies are headed into the best of times. Even in the unlikely event that fuel prices plunge, the spike that has already occurred is sufficient to exacerbate inflation that had already begun to squeeze middle-class Americans hard. Trump keeps promising the pain will end soon, but debt service alone has grown so large that only a catastrophic deflation can purge the financial system of its extreme excesses. The stock market is acting as though everything will turn out right, but, to repeat: the vertical rally is almost entirely short covering, and we should not deceive ourselves into thinking it will end well.

Prop Desk Crooks Take an Unscheduled Breather

It is neither bulls nor bears who move the markets, but crooks, mostly. Spectacular but fleeting rallies draw nearly all of their buying power from panicky short covering that is easily triggered and deftly harvested. I have previously discussed this phenomenon, which is most visible when stocks take unseemly leaps at the opening bell. Although few shares will have changed hands in the gaps this creates on charts, it effectively fattens the bank accounts of everyone who held stock before the leap.

How do the thieves (aka ‘broad-tossers’; see photo above) who control the markets do this trick? First, in order to deplete sellers, they pull their bids in the wee hours of the morning. When there is no news of special interest, stocks will tend to drift lower, especially if there are no significant buyers on the way down. The trend will begin to feed on itself as shareholders grow uneasy. If Wall Street’s Wharton-educated crooks have orchestrated the heist properly, a selling crescendo will cause stocks to bottom about 30 to 60 minutes before the start of the regular session.

Then, with sellers exhausted and no offers in sight, it is bears who will start to grow anxious. Their increasingly urgent bids to close out short positions will continue to accumulate as the opening approaches. It is then that the Masters of the Universe, mainly specialists licensed to maintain orderly markets, but also to steal from amateurs, will spring the trap, pulling their offers to reset prices to a level that can satisfy pent-up demand. That price will often be well above the previous day’s close. Voila! Instant new $$ billions for the white-collar carnies who operate the world’s bourses.

Why Stocks Idled

The foregoing helps explain why stocks did nothing on Friday. Until a few months ago, before the bull market sputtered out, Fridays were usually a celebratory day when bears were too scared to get in the way of the stampede. Lately, though, this has changed, since there is less bullish news to boost markets. And even when the news is ostensibly good, such as the recent announcement of a cease-fire with Iran, there are sufficient doubts about the veracity of the headlines to dampen the enthusiasm of buyers.

Not that good news is necessary to send stocks soaring; the mere absence of bad news will usually suffice. Regardless, for the thimble-riggers, the idea is not to buy low and sell high on good-news days, but to slingshot stocks in both directions with such ferocity that entering and exiting at the intraday extremities is the quickest and surest way to rack up sensational gains. Of course, it helps if you can see the order book, which is as good as a crystal ball for predicting exactly when buying or selling will dry up.

Card Mechanics

On Friday, exchange markets that typically grow feistier with the approach of the weekend traced out a brain-dead sine wave that would have suffocated any trader trying to leverage price swings. Headlines from a day earlier were starting to molder on the vine, mostly with ignorant speculation about who is winning the war. That kind of non-news is hardly conducive to slingshotting stocks around, and so the supposed Masters of the Universe lay exposed for a few hours as the one-trick sleazeballs they are, unable to act when there was no news to turn the herd crazy.

Rick’s Picks nevertheless left subscribers with a moderately bullish bet designed to capture some of the ginned-up energy if the ass bandits should trigger off a short squeeze early this week. They have treated the war as a mere annoyance and are anxious to get back to business as usual. That means enriching themselves by jump-starting the flow of Other People’s Money into stocks. However, we seriously doubt they will achieve new record highs this time, so don’t get carried away if you have access to our strategy. And speaking of getting carried away, here’s a link to our latest interview with Howe Street’s Jim Goddard. This is not-ready-for-prime-time stuff that even the most brazen Fleet Street tabloid would think twice about publishing. (One of my favorite teaser headlines, from rock music’s heyday in the late 1960s, was this one from a British tabloid, Melody Maker: “Tits, Ass and Hot Revolution Inside…”) [The author was a market maker on the floor of the Pacific Stock Exchange for 12 years.]

A Dreadful ‘What If’ Could Turn the Bear Savage

Did you fade the Dow’s 1100-point rally on Tuesday, or the nearly 500-point follow-through the next day like I told you to? I’d written here a few weeks ago that shorting into strength these days offers the best odds bears have gotten in decades. Stocks had spent four months building an obvious top, and finally, there it was, a precipitously weakening market staring us down just as the U.S. joined Israel in a war against Iran. Usually Wall Street loves nightly footage of an enemy’s buildings getting blown to smithereens by F-35s. The fighter jets cost $100 million apiece, and maintenance and operational costs can add another $300 million to that. But this war has another cost, and it’s not the ‘good’ kind: a huge leap in the price of crude oil and natural gas. Investors go to sleep every night praying something will happen soon to ease the situation. It has pushed gas prices as high as $6 a gallon in California and is threatening to send already steep increases in the price of everything else out of control.

The graph says Wall Street ought not get its hopes too high for quick relief, since crude looks like it could rise to the sky before quotes settle back to a more normal $70 or so someday. But how will Wall Street react if prices reach the $125-a-barrel target in the graph, or maybe even higher? Actually, buyers have shown unmistakable signs of mental illness, but with a seemingly benign twist. Before Tuesday, the broad averages had lurched both ways on a hair trigger, moving inversely with every blip up or down in the price of crude. But on Tuesday they did something so bizarre that no one could have predicted it. With oil up a few dollars, stocks went bonkers, uncorking an 1100-point rally in the Dow. More of this nutty behavior surfaced again on Thursday, which started with oil prices up a whopping 14% overnight. Instead of cowering in fear, however, the S&Ps exploded into a nearly 100-point rally. Crazy, right? Trouble is, the rally came off a deeply oversold low that DaBoyz had engineered ahead of the opening bell. The resulting short squeeze put the S&Ps merely even on the day – still an absurdity considering the dire news from the energy patch.

As Good as It Gets?

That may have been as good as it gets, and our advice is to keep treating every rally like the bear deception it is. One question looms that could have an even bigger negative impact on stocks than rising energy prices or war: Suppose Republicans lose big in November? Even if the GOP is able to hold onto the Senate, the first order of business for a House controlled by the Democrats would be to impeach Trump. He could actually be convicted, possibly with some Republican votes, if the Senate flips to the Democrats. Meanwhile, if stocks continue lower as I expect, and the decline steepens as the election draws closer, you’ll know that the absolutely unthinkable — vengeful Democrats regaining control of Washington — is about to happen. Investors seem not to be paying much attention to this possibility, but it is hardly a longshot, given the tidal shift in the polls of independent voters who evidently have had enough of Trump. When Wall Street wakes up to the implication of this, probably within the next 2-3 weeks, the stock market’s balky feints lower could turn overnight into an avalanche.

The Bear Has Finally Emerged

The war with Iran has put investors in a deepening state of anxiety, since no one can say for sure how things will turn out. Wall Street’s obsessive focus has been on the price of oil, implicitly trusting that the supposed collective wisdom of markets is superior to whatever information we could glean from headlines and op-ed pages. The trouble is, the story that crude oil spins each day mutates with wild price swings that suggest the markets are an idiot, as clueless as we are.

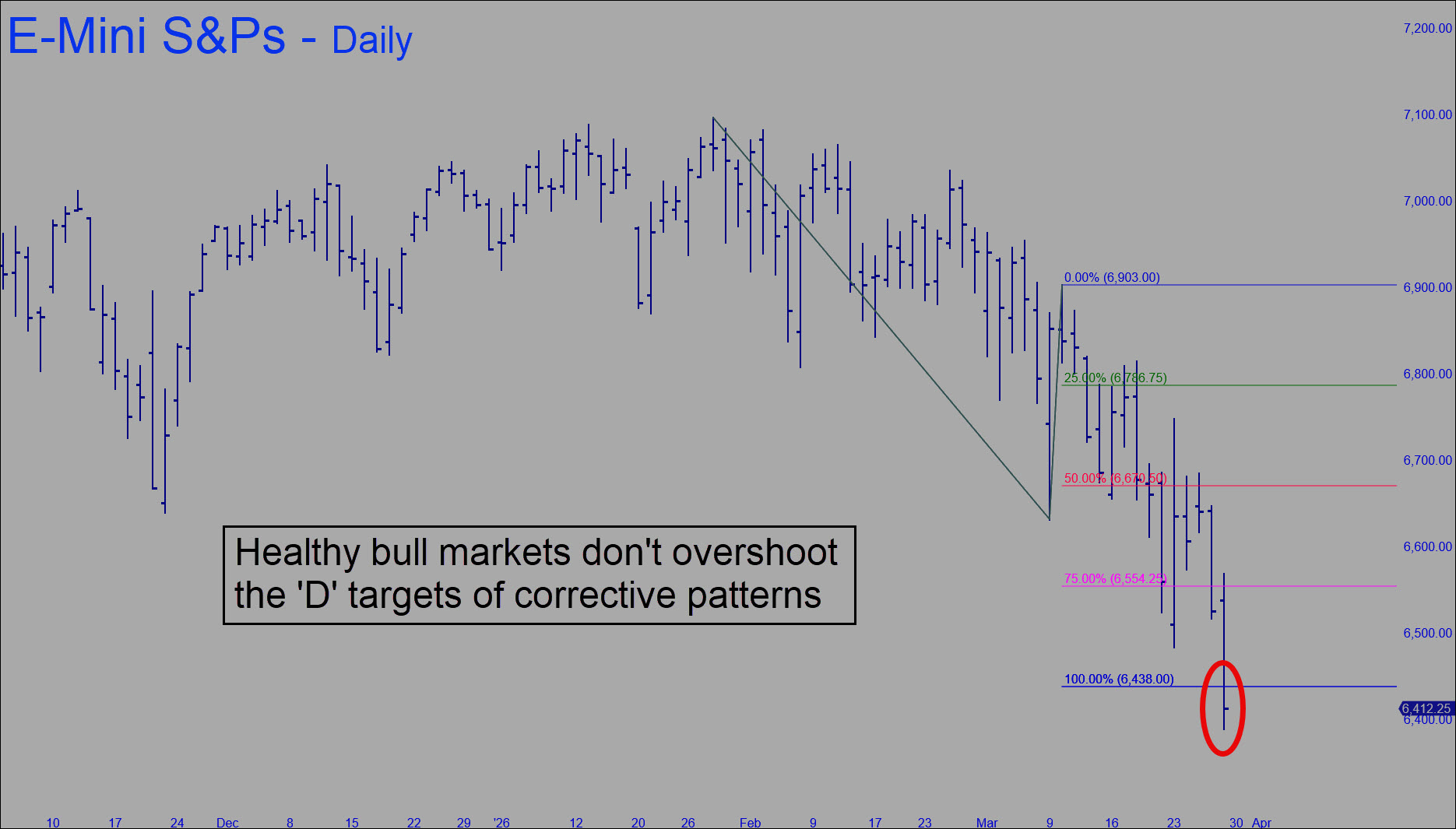

The charts I use to get a tight handle on the stock market are less confusing, however, and they are saying unequivocally that the bull market begun in 2009 is over. To state this in a disinterested, technical way, when ABCD corrections in bull markets start exceeding their ‘D’ targets, as occurred last week in the S&Ps, the major trend has changed.

The small target-overshoot in the E-Mini S&P chart above tells us more about the stock market’s health, or lack thereof, than a cacophony of pundits and eggheads ever could. It says a bear market that has always been inevitable has finally begun. This will also mark the end of Trump’s heroic run, negating his magical ability to move the markets and to persuade people that everything will turn out okay if we just give it more time.

Trump’s Miracles

It is difficult to criticize a man who has produced so many political and geopolitical miracles. Admittedly, we have never believed in the economic kind, since Americans are much too deeply in debt to escape a Second Great Depression. When it comes, it will take down a global regime that has come to depend on America’ economic strength and, more recently, its leadership.

The hope remains that Trump will put our domestic house in order before systemic failure makes the task impossible. Although he might not succeed in putting Hillary, Comey, Schiff, Brennan, Clapper, Obama, Biden and all the others on trial, by exposing their treachery he has dealt a mortal blow to their ceaseless efforts to subvert the Republic.

Missile Threat Eclipses ‘Investable Ideas’

Although Trump has achieved many spectacular successes in his second term, he has made two big promises he can’t possibly keep. The first was to bring back affordability to the broad middle class. Anyone who believes this must be living on some planet with an all-powerful ruler who generously provides everyone with low-cost homes, apartments, childcare, senior care, pet care, car repairs, college tuition, groceries and insurance. Trump’s second promise is that he will wind down the Iran war quickly. This ranks right up there with George W. Bush’s ‘Mission Accomplished’ speech in 2003, when major combat operations in Iraq turned out to have been far from over. Few took him seriously at the time, just as few believe Trump is close to bringing the mullahs to their knees.

Far from surrendering, they reportedly have been pondering whether to attack Israel’s Dimona reactor, a key facility in the nation’s nuclear weapons program. The town of Dimona was hit by a powerful missile over the weekend, but if Iran targets the reactor, that could conceivably release radioactive material into the atmosphere, threatening not only to kill all human life in the region, but throughout the world. If Israeli were to retaliate proportionately, the destruction this could cause lies beyond imagining.

The Annihilation Trade

I usually try to focus on investable issues in these weekly commentaries, but they are less-than-trivial in comparison to a nuclear threat that could annihilate mankind. No one doubts that Iran’s leaders are fanatics who are capable of doing anything to avoid defeat. This threat is not going to go away, nor are oil prices going to retreat any time soon. With interest rates rising, a pumped-up stock market and feverish global economy are facing a perfect storm. If you are looking for a trade, there is probably no time in the last hundred years when it was safer to short into rallies. Concerning the steep plunge in gold and silver quotes last week, rest assured that it was engineered by white-collar thieves desperate to shake loose as much supply as they can before investors come to their senses and stampede into the only form of money left in this world that hasn’t been hocked six ways of Sunday.

How a Vacation Resets Your Inner Clock

My regular commentary will resume next week when I my return from a busman’s holiday on the West Coast. In its place is an excerpt from Thomas Mann’s The Magic Mountain that holds an epiphany for the way we experience and recall the passage of time. It has been published here before, but this version was masterfully shortened and simplified by ChatGPT so that more readers could understand and appreciate it. The original can be found in the chapter “Excursus on the Sense of Time” in several translations. RA

There is something peculiar about deliberately settling into a new place—making the effort to adjust, to feel at home—only to leave again once that adjustment is complete. We insert such intervals into our lives as a kind of restorative break. They are meant to refresh us when the steady sameness of daily routine has begun to dull and weaken us. But this dulling is not simple physical or mental fatigue; if it were, rest alone would cure it. The real issue is psychological: when life becomes too uniform, our sense of time fades. And because our awareness of time is bound up with our awareness of being alive, when one weakens, so does the other.

We commonly think that interesting experiences make time pass quickly, while monotony makes it drag. That is only partly true. Monotony does make hours feel long and tedious. Yet over longer stretches it has the opposite effect: it compresses time. Large, uniform periods shrink in memory until they seem to vanish. By contrast, rich and varied days may fly by in the moment, but they give weight and substance to life as a whole, so that years filled with variety seem fuller and longer than empty ones that slip away unnoticed.

Sameness Brings Tedium

Tedium, then, is not the lengthening but the abnormal shortening of time tough sameness. When every day resembles the next, they collapse into one; complete uniformity would make even a long life feel brief, as if it had stolen past us. Habituation is a kind of sleep of the time-sense. This is why childhood seems long, while later years accelerate.

We therefore seek change and novelty to revive our sense of time and, with it, our sense of life. Travel, cures, holidays—these work because new surroundings broaden time’s flow. The first days in a new place feel expansive, perhaps for a week. Then familiarity sets in, and time begins to contract again. Anyone who clings to life can feel how, toward the end of a stay, the days grow lighter and scurry past like dry leaves.

The effect lingers briefly after returning home: the first days back feel fresh and spacious. But we adapt more quickly to the ordinary than to the exceptional. If age—or low vitality—has already weakened the sense of time, the renewal fades almost at once. Within a day it can feel as though we had never left at all, as though the journey were no more than a brief watch in the night.