Although we featured pithy weekly commentaries in this space for many years, the time and effort spent crafting them is now devoted to making the Rick’s Picks Trading Room an unbeatable source of timely trading ideas for novices and professionals. You should check here weekly, since I will continue to post links to my latest interviews and to offer visual enticements designed to entertain, amuse and enlighten you. Much of it will come from YouTube, since their video catalog is endlessly fascinating. Submissions, including home videos, are welcome and should be sent to this address. To get things rolling, click here for an unbelievable drum solo that demonstrates why the late Buddy Rich would never have worried about being replaced by a synthesizer. The headline is the title of one of his many albums.

Subscribe Free!

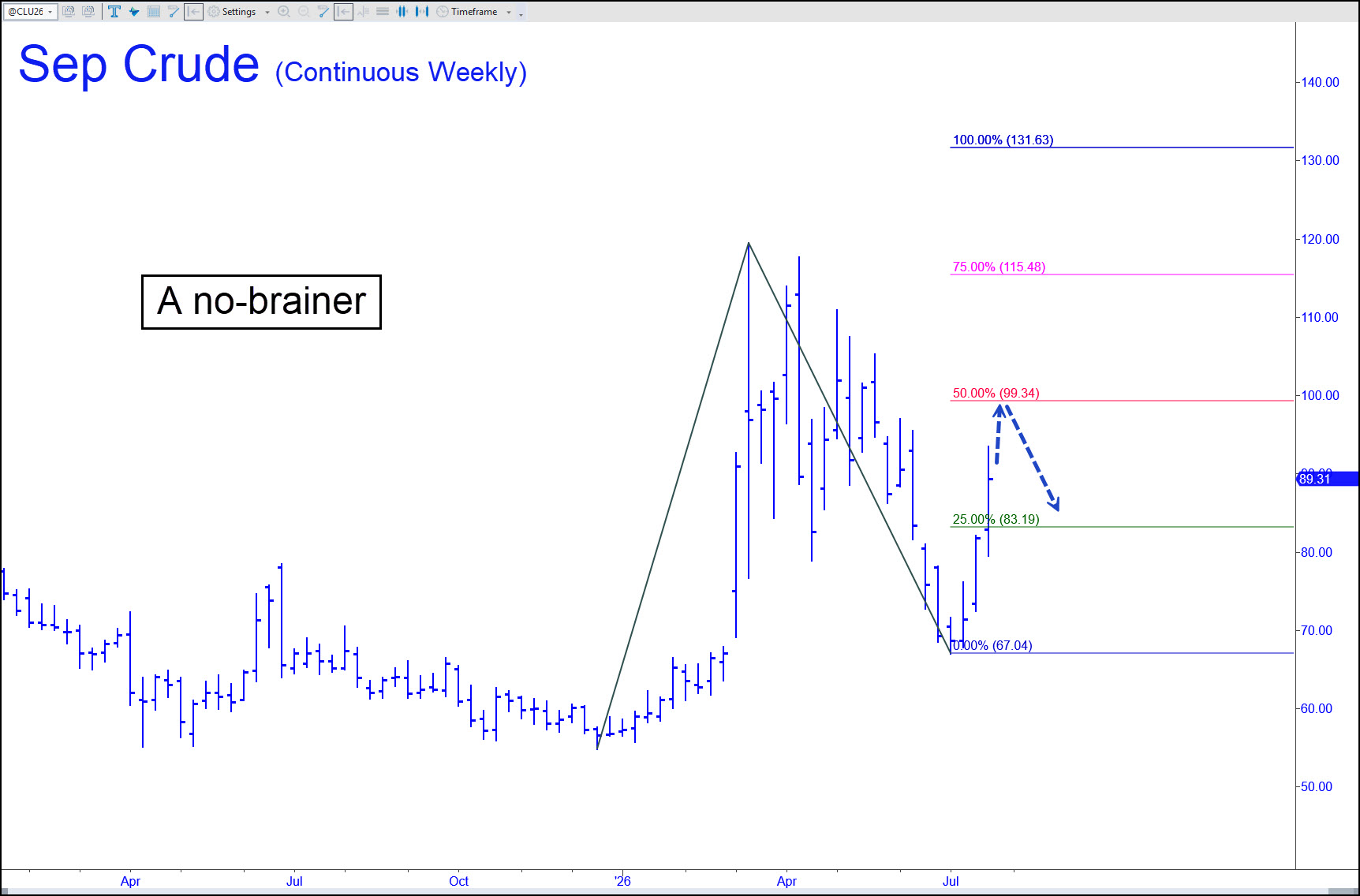

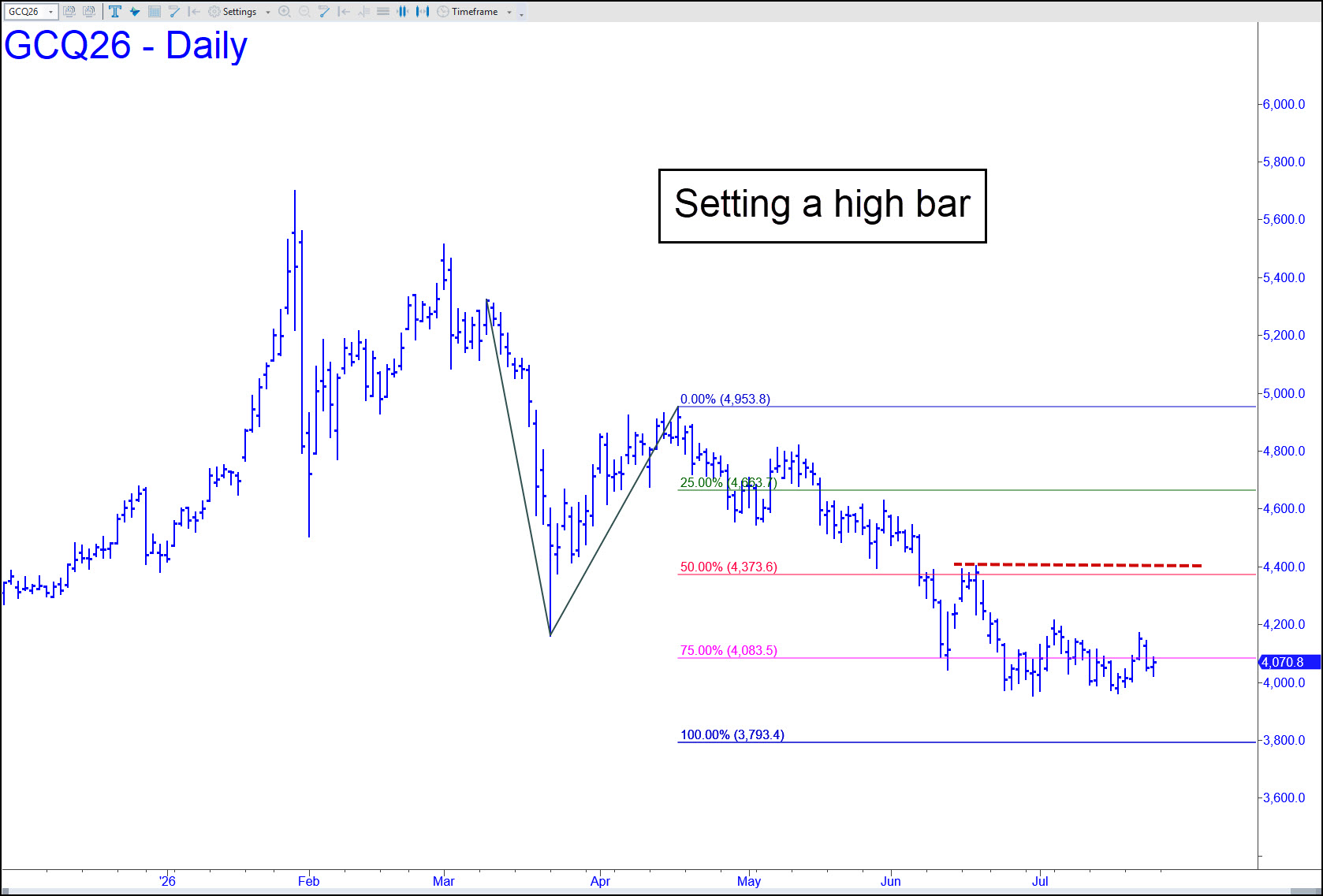

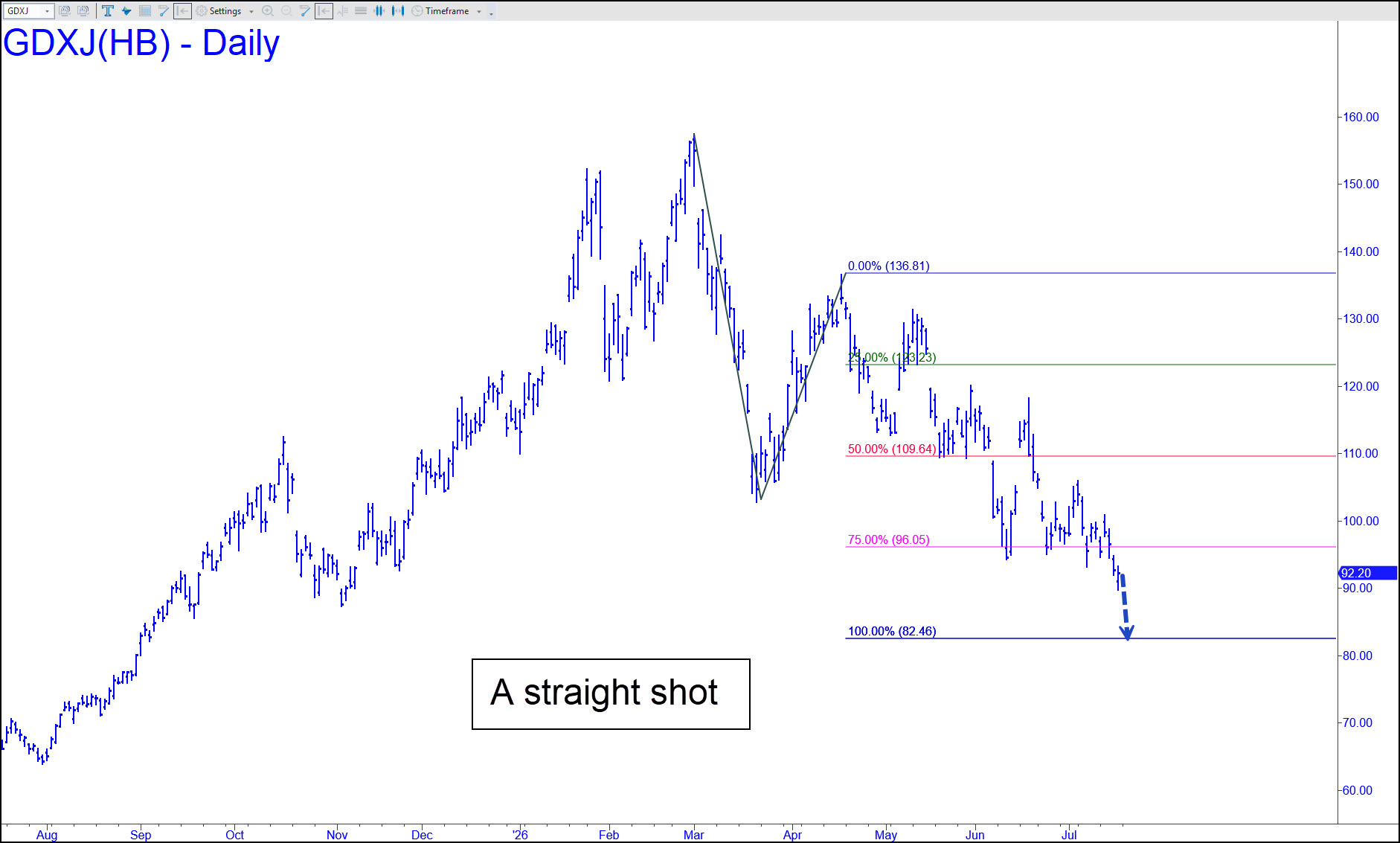

The analytical ‘touts’ below, overhauled each Sunday and updated 24/7, will continue as always, as will their barbed emphasis on the similarities between Wall Street and sleazy carnival midways. The remarkable accuracy of our trend calls and price targets is a matter of daily record and must be observed up close to be believed. Sign up for a free trial with access to all site amenities by clicking here (no credit card needed). Then click here for my most recent interview with Howe Street’s Jim Goddard. We talk about the Information Age and whether there is enough value in manipulating data to keep America prosperous and to support grotesquely bloated asset prices.

{kind=link}