[Following is a letter that my friend Doug Behnfield, a Colorado financial adviser whose thoughts have been featured here many times before, sent out to clients as the new year began. Doug is an unapologetic deflationist like your editor — a point of view that has served him well in recent years. Although February has been disappointing for investors weighted in long-term bonds, Doug sees them recovering, and yields falling even lower, as the U.S. economy fails to gain strength. For our part, Rick’s Picks has predicted a drop in long-term rates below 2%, and possibly to as low as 1.63%. If so, those who hold T-Bonds and long-term munis stand to reap substantial capital gains, since the longer the maturity, the more leveraged these assets are to even small changes in interest rates. RA]

hope

verb

1. want something to happen or be the case.

“Hang me just ez high ez you please but please don’t fling me in dat briar-patch!”

— Bre’r Rabbit

***

The performance of the bond market in 2014 took practically everyone by surprise (except for yours truly and a few money managers like my friends at Hoisington Management). Here is an excerpt from a great article in the New York Times that tells the tale: “For Bond Investors, That Other Shoe Still Didn’t Drop”:

“If you asked anyone at the beginning of 2014 where the rate on the 10-year Treasury would end the year, I don’t think anyone would have said lower, and most would have said one percentage point higher,” says Stephen Kane, a group managing director at TCW, which manages $110 billion in fixed-income portfolios, including the Metropolitan West Total Return Bond fund.

“Yet the bellwether Treasury note ended 2014 at 2.17 percent [it hit 1.72% today] after starting it at 3 percent. And while the United States economy showed some vigor — typically a trigger for rates to rise — global investors fleeing weakness in other markets were eager to buy American bonds. That demand pushed bond prices higher and yields lower.

“The upshot is that last year was frustrating only for the bond bears who have been waiting since 2009 for interest rates to rise from the abnormally low levels manufactured by Federal Reserve policy.”

All the ‘concern’ about inflation that has become such a central theme among Wall Street strategists and economists in the last couple of years is really hope that deflation can be avoided, in much the same way that Bre’r Rabbit feigned fear of being thrown in the briar-patch. When Bre’r Bear and Bre’r Fox fell for it, Bre’r Rabbit scurried away, saying; “Dat’s de place I love de very best. Dat brier-patch is the place where I wuz born!” Investors fell for the popular narrative in 2013 when, between May and September, interest rates spiked and our long-term bond positions got hammered. My outlook at the time was based on the premise that the economy would not achieve “escape velocity,” inflation would not reverse to the upside, and the Fed would not raise interest rates. All of those premises were correct, and so the rise in rates (and the subsequent decline in bond prices) in 2013 turns out to have been a head-fake. It was driven by the hope that the old, pre-2008 credit expansion would resume, even though there was tons of evidence that it would not. Hence the dramatic reversal and recovery in bond prices and the delightful investment performance that is evident in our 2014 returns. There is an old adage that “hope is not an investment strategy” and I believe it. “Escape velocity” is even more unlikely in 2015 than it was in 2014 and the current state of the financial markets argues for staying the course in our long bond positions.

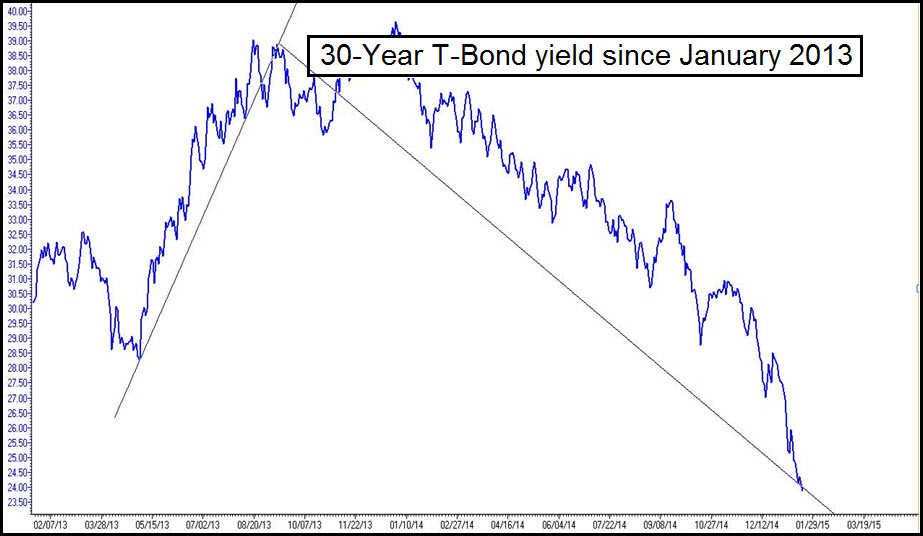

In 2014, the yield on the 30-year Treasury bond dropped from 4% to 2.75%. The 30-year Strip (0% coupon bond) delivered a total return of 50%. The yield on the Barclay’s 22-year and longer Municipal Revenue Bond Index dropped by over 1% and delivered a total return of 15.24%. The average total return for leveraged, long-term closed-end municipal bond funds in the UBS coverage universe was 20.3%.

The decline in long-term interest rates in 2014 (see chart, above) resulted in substantial appreciation in long-term bond prices because, as a reminder, bond prices move inversely to interest rates. In order to calculate total return, the current yield must be added to the price appreciation. For example, the 20.3% total return on the typical closed-end muni fund was a combination of about 7% in tax-exempt interest income and 13% in price appreciation.

Long-Term Performance

As long as I am doing the primer thing, this year’s great performance in the bond market needs to be put in the perspective of our long-term annualized performance. In 2013 (when interest rates spiked) the performance of accounts that were positioned with long-term bonds as the predominant allocation had negative returns and this year, they had positive returns. If you put the 2 years together, you get an annualized return that is fairly moderate. Long-term investment performance is similar in some ways to maintaining a GPA in college. It requires an enormous amount of effort (and fast) to recover from a “lost” semester.

Thankfully, that is exactly what happened. Adding to the college analogy (with a little bit of longing), it is important to learn from our experience. What we wish we knew then is just how big a part of our risk/return profile ‘preservation of capital’ really is. As we get older and wiser and wealthier, we become more defensive. And in the spirit of preservation of capital, bonds are much safer investments than stocks or real estate or collectables. That is because bonds are guaranteed. Someone guarantees the “timely payment of principle and interest” on each and every bond and that guarantee is particularly solid if the guarantor is a municipality or the Federal Government. Adding to the appeal of bonds is the fact that the risk is relatively simple to monitor: If rates go up, bond prices go down. If rates keep going down, our portfolios continue to appreciate.

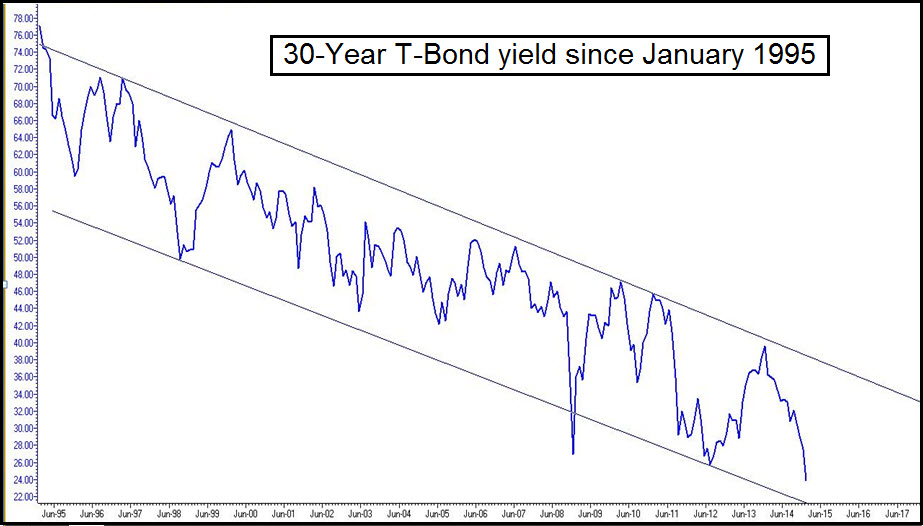

Over the very long term, the deciding factor for investment grade bond yields has been primarily the rate of inflation. And interest rates have been going down along with inflation for the most part since 1981. For the past 34 years, the risk for fixed income investors has been not owning bonds with maturities that were long-term enough. That is because shorter term fixed income vehicles have delivered continuously lower rates of interest (and income) and now we are at the point that even a two- year CD pays but 1%. Long-term bonds have provided stable cash flow and meaningful appreciation to offset the decline in interest rates.

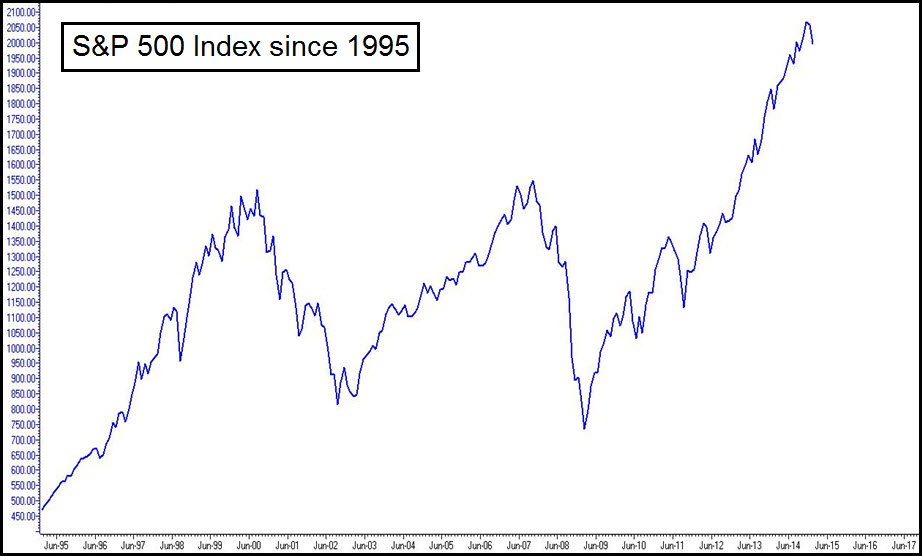

S&P 500 Uncorrected Since 2011

The last time the equity market (as measured by the S&P500 Index) had a down year was 2008, when it declined 38% before dividends. There has not been as much as a 10% correction since 2011, and those statistics alone suggest that something in the way of a significant decline is overdue. If such a decline were to occur in the future, it is likely that the deflationary impact of lower stock prices would lead to even further declines in the rate of interest paid on long-term government bonds and prices would continue their ascent.

The recent acceleration of the decline in interest rates is widely attributable to plummeting oil prices, weak global consumer price inflation (or actual deflation in some countries), and sluggish global economic growth. The stickiness of stock prices near the all-time highs makes them the “odd man out,” along with the price of fine art, collectibles and high-end residential real estate.

What’s Next?

The important topic to hit in these year-end comments, as always, is “What’s next?” Bond prices have benefited from a long list of deflationary events in the past year. The dramatic decline in oil prices is the poster child. But will deflationary events continue to dominate the global economy in the coming year? It seems likely. And, as a result, we should maintain our bullish stance toward high quality long-term bonds and avoid investment assets that are vulnerable in a deflationary environment.

Today, the yield on the 30 year Treasury bond made an all-time low of 2.36%. As promised, we are lightening up a little on our long-term Treasury Strips, in favor of select alternative investments and bonds that have a better current yield and somewhat less risk in the event that rates do reverse to the upside. In many ways, the bond market is shaping up like it did in December of 2008, when David Rosenberg published “Saying Good-bye to an Old Friend” while Chief North American Economist at Merrill Lynch. At the time, we determined that Treasury bonds had reached the low yield levels that we thought they would, but we were not bearish. We just thought that the opportunity was better in some other areas of fixed income, particularly closed-end municipal bond funds, which were trading at substantial discounts. At the time, they offered the “margin of safety” that we were looking for but they appeared to have much more potential for capital appreciation. It was a spectacular market call then and it is shaping up to be a similar opportunity in today’s market environment.

Mava,

It is quite sobering to realize we are now at the point where no one is talking along the lines of bringing about change in America.

Only about how the Oligarchs will consolidate their grasp on wealth and power, and how long it will take them to do that.

Hillary or Jeb?

Two sides to the same coin.

Heads they win.

Tails we lose.

I expect to see Warren Buffet, the Walton Family, and the Koch Brothers all to receive the Presidential Medal of Freedom for their contributions to America in the near future!

And to receive lands and titles to fit their status as Feudal Overlords of the Realm!

Glacier National Park, Yosemite, and Redwood National Park would seem appropriate rewards for these Economic Patriots!

Naturally!