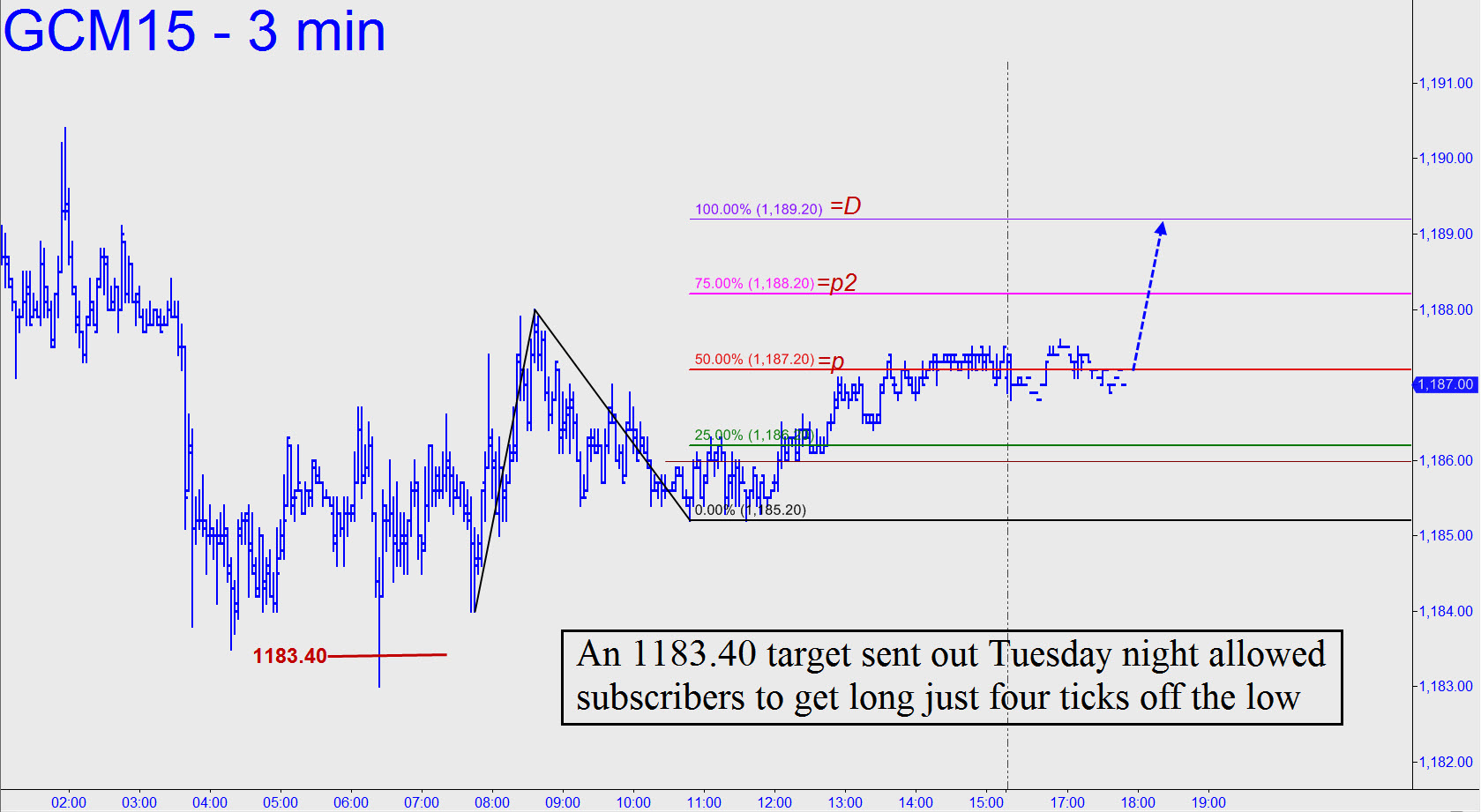

The 1183.40 downside target given here yesterday allowed subscribers to get long four ticks off the intraday low. Since I received reports of actual fills in the chat room, I’m establishing a tracking position: long two contracts with a cost basis of 1180.90. That’s based on an initial purchase of four contracts, with half exited at 1186.00, the approximate midpoint of the 5-point rally that ensued. For now, we’ll look to exit a third contract three ticks below the 1189.20 target shown, at 1188.90. For now, make the order o-c-o with a stop-loss on the entire position at 1184.80. If you hold just a single contract, an ‘impulsive stop-loss’ would imply exiting at the same price, 1184.80. At or above the pink line (p2=1188.20), you should switch to a ‘dynamic’ trailing stop that shrinks as 1189.20 is approached so that risk:reward is held constant at 1:3. If the futures surge higher, exceeding 1190.40, consider sticking with the position. _______ UPDATE (9:28 a.m. EDT): A spike overnight to 1192.00 made it possible to exit a third contract at 1188.90, as suggested above. This would have produced a gain of $800 and left a single contract with an 1180.90 cost basis. It should have been sold at around 6 a.m. for 1186.80 when the futures went bearishly impulsive on the intraday charts. The total gain worked out to a theoretical $1400 for a position held less than a day. FYI, the monthly composite chart says the June contract must fall to 1094.00 over the next four to six weeks before it finds good traction. P=1200.90, but so far price action has not been conducive to a mechanical short there. (A= 1346.80 on 7/31/14).

The 1183.40 downside target given here yesterday allowed subscribers to get long four ticks off the intraday low. Since I received reports of actual fills in the chat room, I’m establishing a tracking position: long two contracts with a cost basis of 1180.90. That’s based on an initial purchase of four contracts, with half exited at 1186.00, the approximate midpoint of the 5-point rally that ensued. For now, we’ll look to exit a third contract three ticks below the 1189.20 target shown, at 1188.90. For now, make the order o-c-o with a stop-loss on the entire position at 1184.80. If you hold just a single contract, an ‘impulsive stop-loss’ would imply exiting at the same price, 1184.80. At or above the pink line (p2=1188.20), you should switch to a ‘dynamic’ trailing stop that shrinks as 1189.20 is approached so that risk:reward is held constant at 1:3. If the futures surge higher, exceeding 1190.40, consider sticking with the position. _______ UPDATE (9:28 a.m. EDT): A spike overnight to 1192.00 made it possible to exit a third contract at 1188.90, as suggested above. This would have produced a gain of $800 and left a single contract with an 1180.90 cost basis. It should have been sold at around 6 a.m. for 1186.80 when the futures went bearishly impulsive on the intraday charts. The total gain worked out to a theoretical $1400 for a position held less than a day. FYI, the monthly composite chart says the June contract must fall to 1094.00 over the next four to six weeks before it finds good traction. P=1200.90, but so far price action has not been conducive to a mechanical short there. (A= 1346.80 on 7/31/14).