The Bear Has Finally Emerged

The war with Iran has put investors in a deepening state of anxiety, since no one can say for sure how things will turn out. Wall Street’s obsessive focus has been on the price of oil, implicitly trusting that the supposed collective wisdom of markets is superior to whatever information we could glean from headlines and op-ed pages. The trouble is, the story that crude oil spins each day mutates with wild price swings that suggest the markets are as clueless as we are.

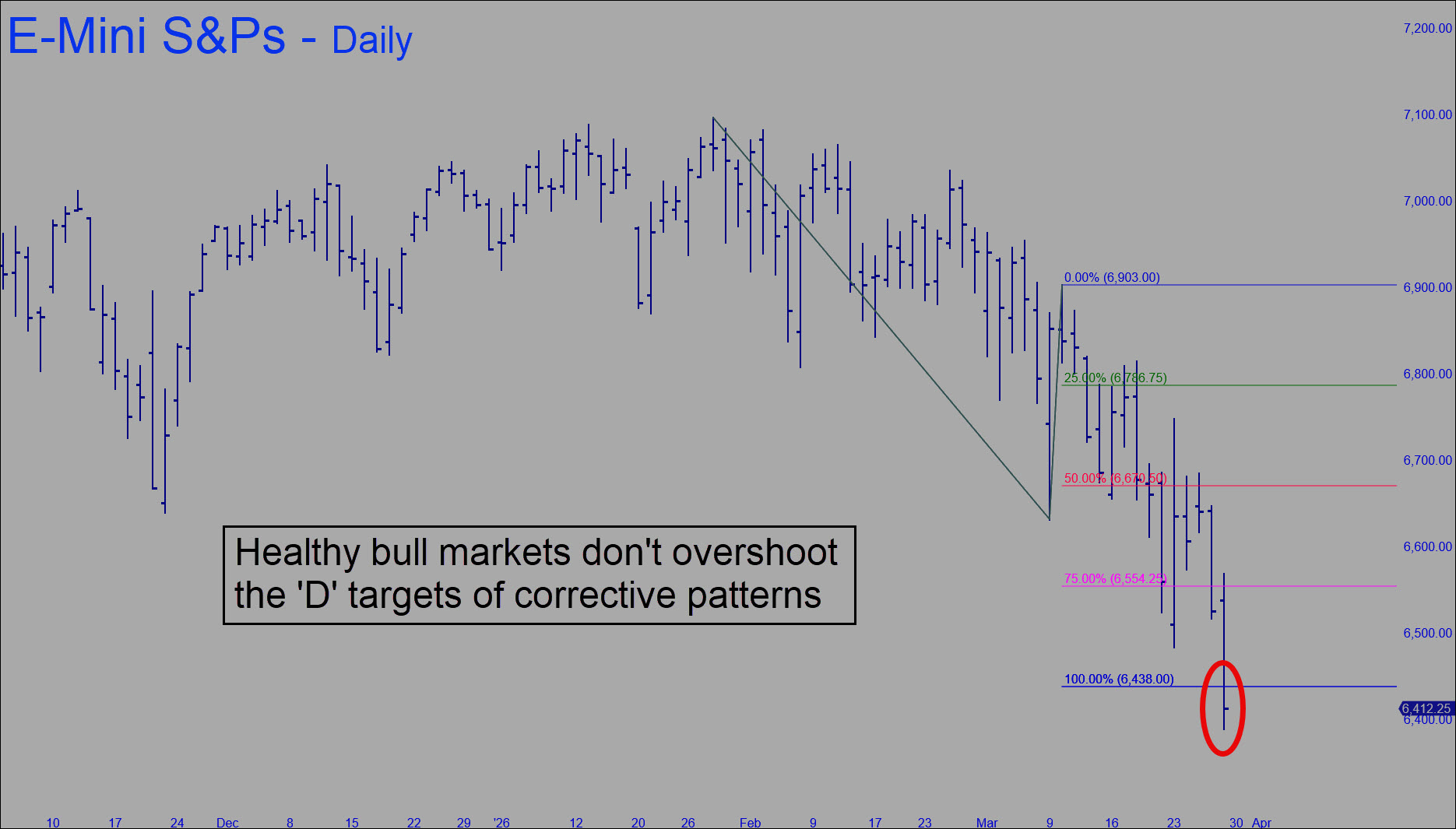

The charts I use to get a tight handle on the stock market are less confusing, however, and they are saying unequivocally that the bull market begun in 2009 is over. To state this in a disinterested, technical way, when ABCD corrections in bull markets start exceeding their ‘D’ targets, as occurred last week in the S&Ps, the major trend has changed.

The small target-overshoot in the E-Mini S&P chart above tells us more about the stock market’s health, or lack thereof, than a cacophony of pundits and eggheads ever could. It says a bear market that has always been inevitable has finally begun. This will also mark the end of Trump’s heroic run, negating his magical ability to move the markets and to persuade people that everything will turn out okay if we just give it more time.

Trump’s Miracles

It is difficult to criticize a man who has produced so many political and geopolitical miracles. Admittedly, we have never believed in the economic kind, since Americans are much too deeply in debt to escape a Second Great Depression. When it comes, it will take down a global regime that has come to depend on America’ economic strength and, more recently, its leadership.

The hope remains that Trump will put our domestic house in order before systemic failure makes the task impossible. Although he might not succeed in putting Hillary, Comey, Schiff, Brennan, Clapper, Obama, Biden and all the others on trial, by exposing their treachery he has dealt a mortal blow to their ceaseless efforts to subvert the Republic.

Missile Threat Eclipses ‘Investable Ideas’

Although Trump has achieved many spectacular successes in his second term, he has made two big promises he can’t possibly keep. The first was to bring back affordability to the broad middle class. Anyone who believes this must be living on some planet with an all-powerful ruler who generously provides everyone with low-cost homes, apartments, childcare, senior care, pet care, car repairs, college tuition, groceries and insurance. Trump’s second promise is that he will wind down the Iran war quickly. This ranks right up there with George W. Bush’s ‘Mission Accomplished’ speech in 2003, when major combat operations in Iraq turned out to have been far from over. Few took him seriously at the time, just as few believe Trump is close to bringing the mullahs to their knees.

Far from surrendering, they reportedly have been pondering whether to attack Israel’s Dimona reactor, a key facility in the nation’s nuclear weapons program. The town of Dimona was hit by a powerful missile over the weekend, but if Iran targets the reactor, that could conceivably release radioactive material into the atmosphere, threatening not only to kill all human life in the region, but throughout the world. If Israeli were to retaliate proportionately, the destruction this could cause lies beyond imagining.

The Annihilation Trade

I usually try to focus on investable issues in these weekly commentaries, but they are less-than-trivial in comparison to a nuclear threat that could annihilate mankind. No one doubts that Iran’s leaders are fanatics who are capable of doing anything to avoid defeat. This threat is not going to go away, nor are oil prices going to retreat any time soon. With interest rates rising, a pumped-up stock market and feverish global economy are facing a perfect storm. If you are looking for a trade, there is probably no time in the last hundred years when it was safer to short into rallies. Concerning the steep plunge in gold and silver quotes last week, rest assured that it was engineered by white-collar thieves desperate to shake loose as much supply as they can before investors come to their senses and stampede into the only form of money left in this world that hasn’t been hocked six ways of Sunday.

How a Vacation Resets Your Inner Clock

My regular commentary will resume next week when I my return from a busman’s holiday on the West Coast. In its place is an excerpt from Thomas Mann’s The Magic Mountain that holds an epiphany for the way we experience and recall the passage of time. It has been published here before, but this version was masterfully shortened and simplified by ChatGPT so that more readers could understand and appreciate it. The original can be found in the chapter “Excursus on the Sense of Time” in several translations. RA

There is something peculiar about deliberately settling into a new place—making the effort to adjust, to feel at home—only to leave again once that adjustment is complete. We insert such intervals into our lives as a kind of restorative break. They are meant to refresh us when the steady sameness of daily routine has begun to dull and weaken us. But this dulling is not simple physical or mental fatigue; if it were, rest alone would cure it. The real issue is psychological: when life becomes too uniform, our sense of time fades. And because our awareness of time is bound up with our awareness of being alive, when one weakens, so does the other.

We commonly think that interesting experiences make time pass quickly, while monotony makes it drag. That is only partly true. Monotony does make hours feel long and tedious. Yet over longer stretches it has the opposite effect: it compresses time. Large, uniform periods shrink in memory until they seem to vanish. By contrast, rich and varied days may fly by in the moment, but they give weight and substance to life as a whole, so that years filled with variety seem fuller and longer than empty ones that slip away unnoticed.

Sameness Brings Tedium

Tedium, then, is not the lengthening but the abnormal shortening of time tough sameness. When every day resembles the next, they collapse into one; complete uniformity would make even a long life feel brief, as if it had stolen past us. Habituation is a kind of sleep of the time-sense. This is why childhood seems long, while later years accelerate.

We therefore seek change and novelty to revive our sense of time and, with it, our sense of life. Travel, cures, holidays—these work because new surroundings broaden time’s flow. The first days in a new place feel expansive, perhaps for a week. Then familiarity sets in, and time begins to contract again. Anyone who clings to life can feel how, toward the end of a stay, the days grow lighter and scurry past like dry leaves.

The effect lingers briefly after returning home: the first days back feel fresh and spacious. But we adapt more quickly to the ordinary than to the exceptional. If age—or low vitality—has already weakened the sense of time, the renewal fades almost at once. Within a day it can feel as though we had never left at all, as though the journey were no more than a brief watch in the night.

Zuckerberg’s Huge Branding Problem

[Your editor is taking a busman’s holiday in San Francisco. Although trading touts will update as usual and I’ll be active in the chat room, this commentary and the next come from the archive. You can judge for yourself whether they were sufficiently on-target to still be relevant. RA]

Stocks looked leaden as the week ended, adding to the impression that the aging bull market is topping. The Dow tacked on a perfunctory 104 points, or 0.22%, and it wasn’t pretty. There was little life in the lunatic sector (aka ‘the Magnificent Seven’), which until recently could be relied on to celebrate its wildest flights of fantasy on Fridays. The biggest winner in the bunch was META, which rose 1.80% on news that Zuckerberg is having second thoughts about his all-in bet on a metaverse.

If you’re unfamiliar with the term, it refers to a virtual world in which users interact online through avatars. Zuckerberg evidently thought there were hundreds of millions of us, if not billions, eager to escape the pain and drudgery of day-to-day life. He was so certain about this that he changed the name of his company in 2021 from Facebook to Meta. But after sinking $70 billion into the concept, there has been precious little payback. Even more troubling to investors is that there are no obvious ways to make back what has been spent already, nor to recoup any further sums Meta might pour into the idea.

Counting on Investors’ Stupidity

To cover up this boo-boo, and to avoid being thought clueless, Zuckerberg did what any muckety-muck CEO in the digital world would have done: a twisting somersault onto the AI bandwagon. “AI is the most important technology we are working on,” he said, evidently hoping investors have forgotten that he spent the last four years taking pains to separate the supposed;y lucrative potential of metaverse from the vague and so-far profitless promises of AI. This latest statement to the press was a smart move if you believe that the $10 gain recorded by META on Friday was the beginning of a lasting rally. More likely is that it will be reversed on Monday or Tuesday, adding to the disillusionment that has been weighing on the broad averages for the last few months.

Meanwhile, Facebook is stuck with a moniker and a concept that are perceived as dead on arrival. Although Zuckerberg is known as a smooth talker, watching him try to extricate himself from this memic trap promises to be entertaining. Faced with a branding problem that is not merely tricky but potentially fatal, he doesn’t dare return to the name ‘Facebook’, since that would be admitting failure and the stupidity of his biggest-ever idea. But if he changes the company’s name a second time to some as-yet-unclaimed, nebulous variant of AI, he will look like a flake. My guess is that he will stick with Meta, forever associating himself with a virtual Edsel. Like Johnny Cash’s boy named Sue, Zuckerberg will have to work three times as hard to be taken seriously, particularly by his billionaire cohort who are already well aloft in their splendiferous AI hot-air balloons.

Why Stocks Look Like Hell

[Events in the Middle East have overshadowed my narrow economic critique of President Trump in the commentary below. His alliance with Israel to knock out global jihad’s command structure is likely to change the world in ways no one can predict. It will also test the idea that only military might can secure a lasting peace. RA ]

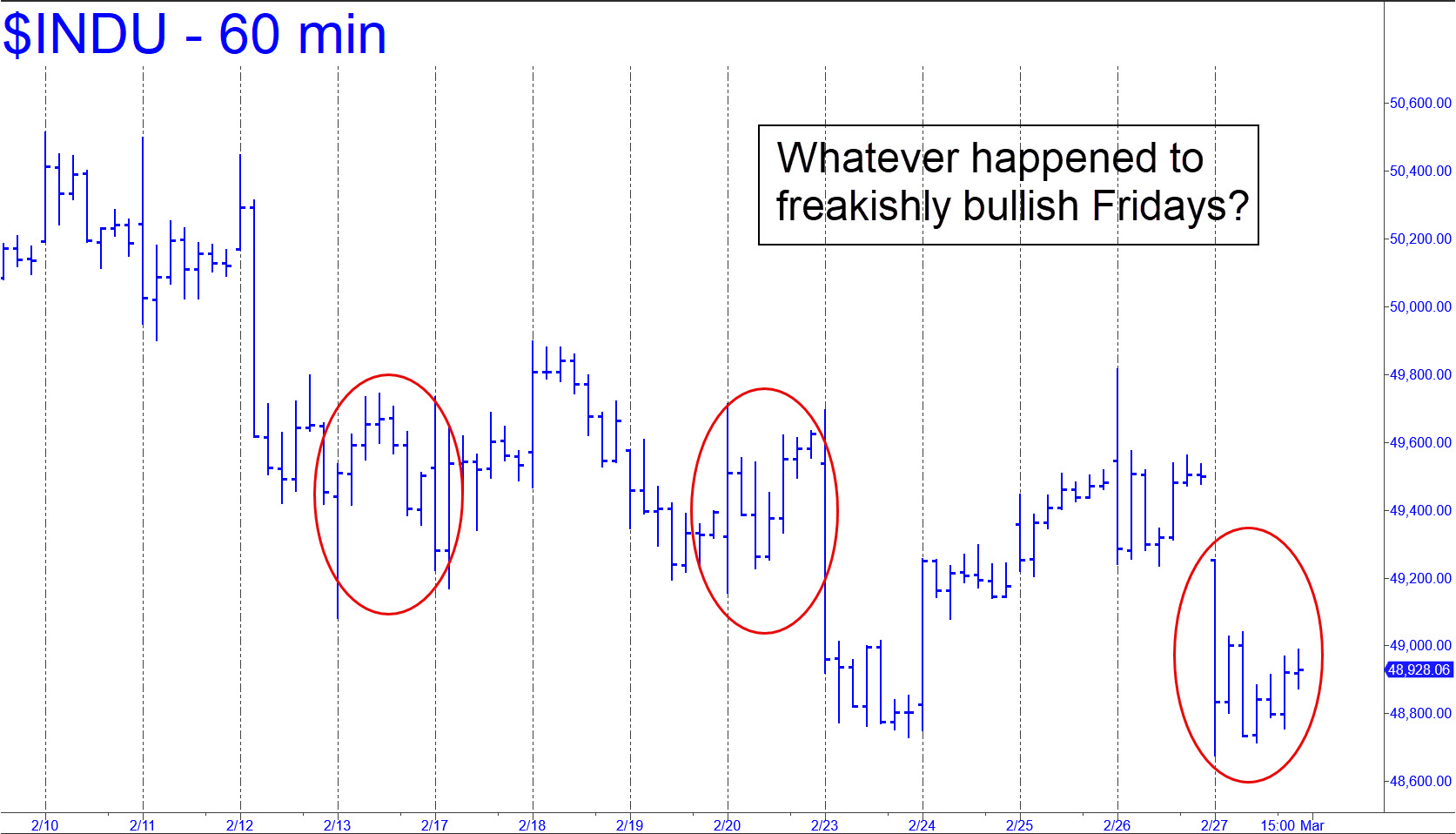

Stocks used to turn feisty toward the end of the week, but as the chart shows, the last few ‘Freaky Fridays’ have been pretty tame. My gut feeling is that this picture of tedium is the calm before the storm, and that stocks are being heavily distributed ahead of a major breakdown. Although I promised a few weeks ago that I wouldn’t mention the words ‘topping process’ again, the alternative would make me sound like a Wall Street shill. The Street’s best and brightest have been flat-out bullish on stocks since the 1929 Crash, having failed to issue a sell signal even on stocks implicated in some of the biggest scandals of the last hundred years. To cite a particularly notorious example, many of them were gung-ho on the shares of Equity Funding until the moment regulators halted trading in the stock one day in March 1973. Read about it here.

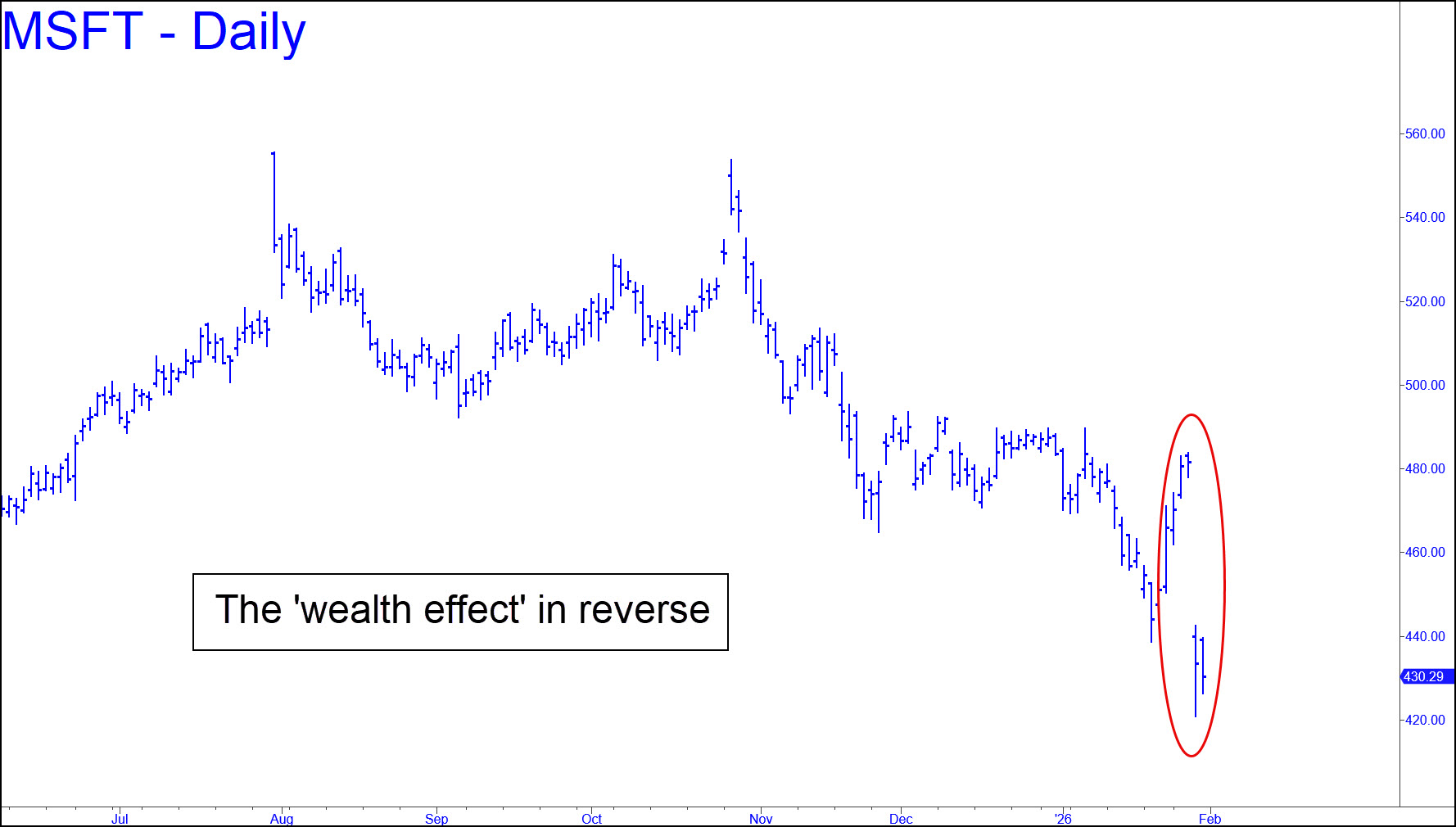

So why have shares been unable to develop a head of steam on Fridays, when irrational exuberance has typically been highest? There are two likely reasons. For one, the AI Bubble has popped. This occurred without much fanfare on January 29, when Microsoft shares dove $60, or 12%, overnight. The shills initially took this for a one-off event, an ‘adjustment’ in the share price of a big company they felt was heavily over-invested in AI. Rick’s Picks saw it as the beginning of the end for AI mania and said so in a commentary out that weekend. Trillions of dollars of valuation have since leaked from the ‘lunatic sector’ (aka the Magnificent Seven) and other stocks, but the deflation is likely to grow much worse before the bloodletting ends.

The second reason shares are acting so punk is that Trumpmania is over. The President effectively killed it with a State of the Union speech last week that bragged about how the economy is going great guns, and how he crushed the inflation caused by his sock-puppet predecessor, ‘Joe Biden’. Any middle-class American who heard the speech recognized it for what it was: more dubious hype than fact. Workers and small-business owners are struggling harder than ever to stay afloat, but inflation is crushing them anyway. And although the cost of eggs, gas and some other staples may have fallen since Trump took office, prices for all the big-ticket items are soaring out of control: health insurance, automobiles, homes, tuition, property insurance, you name it.

Under the circumstances, an exuberant leap to new highs seems most unlikely for the broad averages. The Dow Industrials have eased somewhat after head-butting 50,000 for a few days. DaBoyz are waiting for a news catalyst to drive a short-covering panic. This is the primary force powering all big rallies, the only source of buying strong enough to push stocks past previous peaks and thick layers of supply. If your imagination tells you what bullish news will cause this to happen, then you should be buying stocks hand-over-fist now, not even waiting for a significant dip. I must confess, however, that I am out of ideas. There are plenty of things that could go wrong, though, and the interview I did Friday on This Week in Money discusses them in detail. Click here to access it.

Was China’s Kung Fu Moon-Shot Real?

Robot demonstrations are notorious for going comically awry. Seat Robby at a staged dinner and he will stab himself in the eye with a forkful of make-believe mashed potatoes. Have him put a butter dish back in the refrigerator and he’ll slam the door on his head. So what, then, are we to make of this video, which showcases China’s latest entry in the global competition to build robots that are more human?

Stunning, isn’t it? This is a kung-fu ballet, performed by acrobatic children and a troupe of robots who move with the gracefulness of dancers at the barre. When they abruptly shift gears, vaulting into ten-foot-high somersaults, they land squarely on the rubberized balls of their feet, perfectly balanced. Even more impressive is that there are a dozen of them doing these elaborately choreographed moves in perfect synchronicity.

Search Google for a skeptical take on all this and you have to call up a fifth page of results to find anyone who doubts the video is real. Ever the skeptic, my instinct is to disregard all the oohs and ahhs and focus on the doubters, just as many of us do with product reviews on Amazon. Here’s a jibe on X from an observer who supposedly witnessed a similar demonstration in Shenzen a month earlier: “The [robots were] slow, shaky and could barely shuffle, let alone do any of this. This isn’t the first time [Chinese manufacturer) Unitree has used CGI to fake capability.”

“13 Billion Views”

So who’s telling the truth? It’s an important question, since the video reportedly has attracted 13 billion views so far. That’s according to Chinese news sources, but does the outside world have any reason to trust them? The country’s leaders have a strong incentive to show off the nation’s technological prowess, especially when it is not a nuclear missile glowering at the world from Tiananmen Square. The kung fu demonstration was a very big deal in the world of technology, and if the video was not enhanced, the robots’ performance would be on a par with America’s moonshot in 1969 with Apollo 11.

Even Musk concedes that China is “kicking ass” in humanoid robotics. However, as we went to press, he had not commented publicly on the kung-fu demonstration, which was televised during China’s recent Spring Festival Gala. If the video turns out to have been undoctored, he’ll have his work cut out for him. Is there a cage-fight-of-the-century on the horizon?

Musk Will Be the Last AI Entrepreneur Standing

AI hubris has got itself in a bind, trapped between two conflicting stories, neither of which seems likely to end well. One story has the boys in the billionaire’s club throwing untold sums of money at a technology that seems increasingly unlikely to produce commensurate returns. The other story has been threatening whole sectors of the economy with creative destruction: software development, financial, legal and accounting services, money management, entertainment and even trucking. Each day, there’s a menacing new headline about some industry whose workers, mostly white-collar, are about to be replaced by thinking machines.

The recent trucking news concerned the logistical problem of routing vans so that they are filled with cargo all the time. Artificial intelligence has taken on this challenge, squeezing out inefficiencies in ways that human workers could not have imagined just a few years ago. The shares of companies that do this work crashed last week, victims of AI’s Grim Reaper. It won’t end there, either, since driverless fleets of trucks are coming, and soon. Humans will be needed to load and unload them — that is, until Musk robots come along to relieve them of their jobs.

A Chimpanzee Reflex

Whenever creative-destruction stories hit the tape, the chimpanzees entrusted with America’s 401(k) savings instantly dump the shares of all companies likely to be impacted. The trouble is that the list is growing so fast that it has become hard to imagine an area of the economy that will not be affected. We are talking mainly about job losses, and there seems to be no end to the number and variety of positions in AI’s crosshairs.

So what’s an investor to do? Our money is on Musk, arguably the only player with a strategy imaginative enough to encompass and integrate AI’s myriad possibilities while also tackling its biggest challenges. Some laughed at his demand for a trillion-dollar paycheck, but it grossly understates his ambitions. With plans to be on the moon in just a few years, he is thinking not only outside-the-box, but outside-the-planet. Lunar manufacturing and assembly done by robots will not only solve the problem of how to cool and power GPU server farms, but also provide a low-gravity launching pad to slingshot building supplies to Mars. Humans will get there in rockets, already engineered, that can be refueled and reused within hours of returning to Earth.

Musk has repeatedly demonstrated that he can take multibillion-dollar losses without flinching if an idea hits a dead end. The tens of billions he supposedly overpaid for Twitter has come to seem like relative chump-change for him. And he has the technological means to put Uber, Lyft, Waymo and even Apple out of business in mere months if he wanted to. But he has bigger fish to fry. Musk will be the last man standing when the huge AI shakeout now under way buries the Billionaire Boy’s Club (although not Palantir’s Alex Karp, whose mind is as sharp as Musk’s). Musk makes them all look like amateurs, and the planned merger of SpaceX and xAI, his AI startup, will be the most significant business deal ever hatched. Take a piece of it and you can’t lose. [Here’s a link to my latest interview with Jim Goddard at HoweStreet. The headline alludes to ‘downside targets for silver and gold,’ but that was but a minor concern in this interview. RA]

Time to Jump on the Miners

[The following commentary was written by Steve Houck,a longtime investor in bullion and knows the markets well. He is also a friend and a former business partner. RA ]

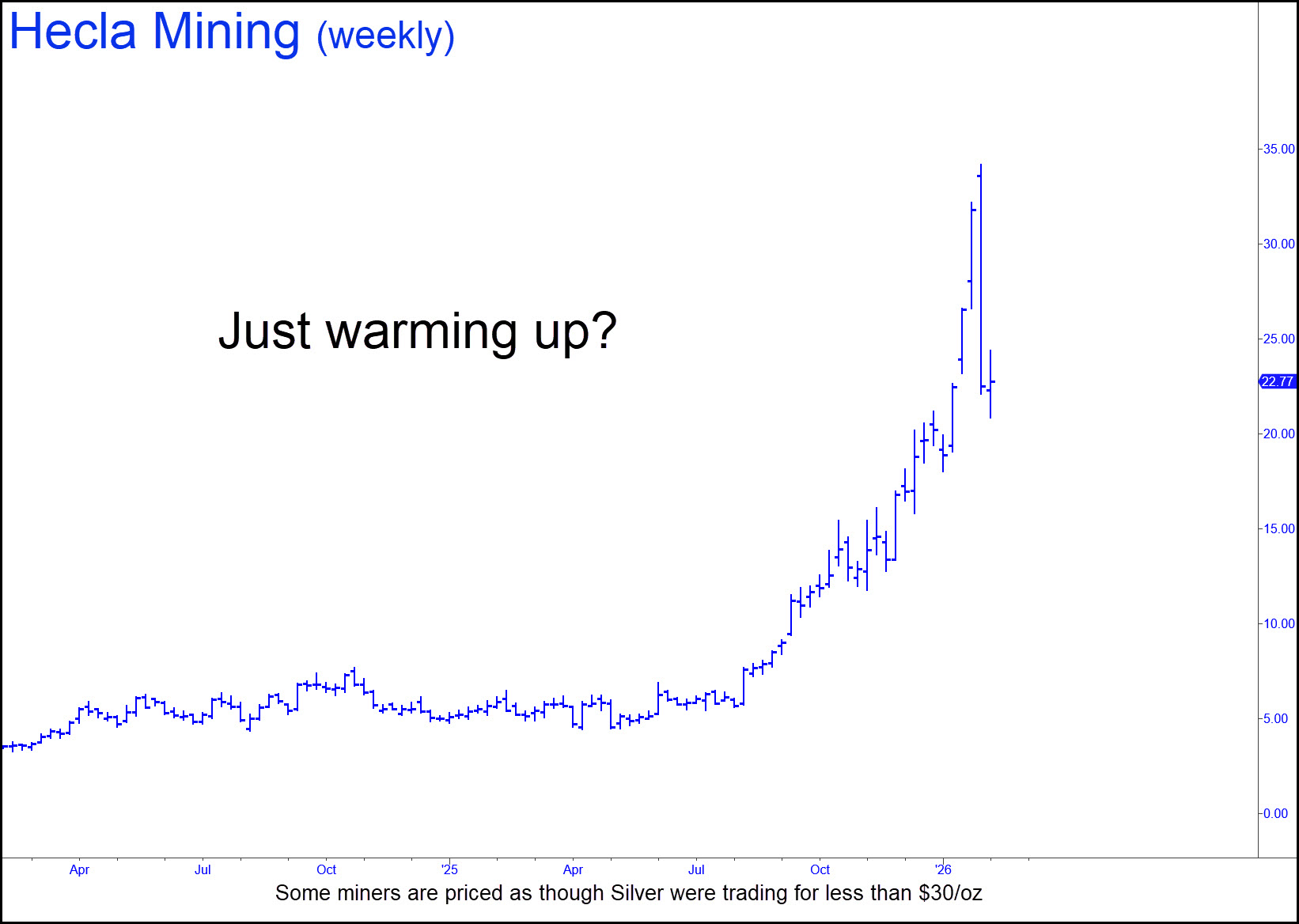

Looking at the froth in silver, it became apparent it was time to rotate from overvalued to undervalued once again. Selling precious-metal ETFs like SLV and AGQ meant cash was available for the next trade, but where to go? While silver has been on a relentless tear, the miners have only grudgingly moved higher. Yes, there have been good moves in many of the miners, but quite a few trade with a ball and chain weighing them down in the form of fear. That’s because the last two times silver surpassed $50, in 1980 and 2011, it collapsed and went into long, grinding bear markets. Silver mining stocks get caught up in this because the public doesn’t believe prices will hold, and that silver will fall back to earth.

But what if the new floor is $55 to $70, and not the $15 to $25 range that obtained for decades? This silver run-up is different because it’s about one thing: physical metal. Just look what;s happening: China, the U.S. and the rest of the world are hoarding and trying to secure metals. That puts the miners in the catbird seat, because they produce and control the supply. Their shares, however, are still being priced as though silver were selling in the $20s even though it averaged close to $50 for the entire fourth quarter 2025. The miners wil start to report earnings next week, beginning on February 16. Because many of them will announce blowout earnings, now is the time to capitalize!

How to Play It

How to play this? Over the last two decades of investing in silver miners, the most important lesson I’ve learned is to stick with producers and developers with projects slated for the near-term. I want the companies I invest in to be extracting metal from the grown now, or within no more than 1-2 years. I start with the major producers and such crowd favorites as Coeur Mining (CDE), Hecla (HL), and Pan American Silver (PAAS). Once I have a good group of the majors, I’ll move to junior producers whose stocks have the potential to appreciate by 500% to 1000%. My largest junior positions are Avino Silver & Gold (ASM), Americas Silver (USAS) and Santacruz Silver Mining (SCZM). These major and junior producers Guanajuato Silver (GVSRF). Silver Storm (SVRS: Vancouver); and Vizsla Silver (VZLA). Here’s a link to comments on ‘X’ that corroborate the essay above with added details.

Microsoft’s Plunge Pricks AI Bubble

Pity the J-school rookies who are paid to explain why the stock market did what it did on a given day. On Thursday, Microsoft shares lost nearly a half-a-trillion dollars of value. But why? Bloomberg’s Evening Briefing called it a ‘rap on the knuckles’ for the company’s huge spending on AI projects that seem increasingly unlikely to pay off. But isn’t a rap on the knuckles the way nuns used to deal with minor behavioral lapses in young boys? If so, then Microsoft deserved 40 lashes with a rattan cane. Although the story was treated by the hacks who wrote it as a news event, what it portends is nothing short of financial calamity, reported in daily installments. For it is not just Microsoft that has squandered hitherto unimaginable sums on failing AI projects, but a dozen other corporate behemoths, including lunatic-sector (aka ‘Magnificent Seven’) stalwarts Amazon, Google, Facebook, Nvidia and Tesla.

Pity the J-school rookies who are paid to explain why the stock market did what it did on a given day. On Thursday, Microsoft shares lost nearly a half-a-trillion dollars of value. But why? Bloomberg’s Evening Briefing called it a ‘rap on the knuckles’ for the company’s huge spending on AI projects that seem increasingly unlikely to pay off. But isn’t a rap on the knuckles the way nuns used to deal with minor behavioral lapses in young boys? If so, then Microsoft deserved 40 lashes with a rattan cane. Although the story was treated by the hacks who wrote it as a news event, what it portends is nothing short of financial calamity, reported in daily installments. For it is not just Microsoft that has squandered hitherto unimaginable sums on failing AI projects, but a dozen other corporate behemoths, including lunatic-sector (aka ‘Magnificent Seven’) stalwarts Amazon, Google, Facebook, Nvidia and Tesla.

Analysts have projected total global AI spending of $2.6 trillion across all companies and markets in 2026. Here’s where the math gets interesting. Microsoft share of those outlays would be an estimated $140 billion. Investors knocked three times that from the company’s valuation last week, while also imploding the world’s gaseous ‘wealth effect’ by a rich but still-invisible multiple. If equal punishment were to be inflicted on the companies planning to spend the $2.6 trillion, the haircut would amount to nearly $8 trillion. That is arguably the approximate size of the AI deflation that lies just ahead, and it will activate a black hole that could double or triple losses in other classes of investible assets. Treasury paper will go bounding in the other direction, finally getting some respect as a safe haven.

When to Take Heart

Granted, neither the math nor the logic is airtight. But the $8 trillion guesstimate is probably more credible than the rap-on-the-knuckles summation offered by Bloomberg. Their reporters are too lazy and too poorly trained to attack the real story, which will soon spread far beyond Microsoft. As it develops, and stocks begin to fall with increasing momentum, the op-ed columnists will catch the scent of panic and write more explicitly about the AI bubble’s collapse. Reporters will eventually follow suit, and that’s when you can take heart, since the bear market will be half-way to a bottom by then. (Click here for my latest interview — “Let it all hang out!” — with Jim Goddard at Howe Street.)

What Rough Beast?

If you can’t guess what commodity the chart shows, you must be living on Mars. It is in fact a long-term picture of silver, which went ballistic in December. The price has doubled since, blowing out a $50 top that had stood since 1980. That price became a part of silver’s legend, since it is where one of the wealthiest men in the world, oil tycoon Nelson Bunker Hunt, met his financial Waterloo. With his brothers, Lamar and William, ‘Bunky’ had attempted to corner the market by buying up silver and futures contracts amounting to about a third of the world’s supply. Comex regulators responded by raising margin requirements so high that there were just two players left in the game: the Hunts and Eastman Kodak, a huge industrial user of silver. From a record $50.45 per ounce, the price plunged by half in mere days, forcing the Hunts to sell nearly everything they owned to meet margin calls. In retrospect, they seem not to have broken any rules. However, the Comex was forced to crush them in order to stabilize the metals market.

If you can’t guess what commodity the chart shows, you must be living on Mars. It is in fact a long-term picture of silver, which went ballistic in December. The price has doubled since, blowing out a $50 top that had stood since 1980. That price became a part of silver’s legend, since it is where one of the wealthiest men in the world, oil tycoon Nelson Bunker Hunt, met his financial Waterloo. With his brothers, Lamar and William, ‘Bunky’ had attempted to corner the market by buying up silver and futures contracts amounting to about a third of the world’s supply. Comex regulators responded by raising margin requirements so high that there were just two players left in the game: the Hunts and Eastman Kodak, a huge industrial user of silver. From a record $50.45 per ounce, the price plunged by half in mere days, forcing the Hunts to sell nearly everything they owned to meet margin calls. In retrospect, they seem not to have broken any rules. However, the Comex was forced to crush them in order to stabilize the metals market.

What Does It Mean?

Silver’s current rise has been orderly, more or less, but with a pitch so steep that it caught many players with their pants down. No reason to feel sorry for them, since they are ethically and morally on a level with child molesters, broad-tossers and cannibals. But the radical shift in precious-metal prices relative to all other classes of investable assets raises a question that should concern us all. For it is not happening in a vacuum, and we can only guess at what it will mean years down the road. Will silver resume a monetary role? Is Trump licking his chops over the prospect of borrowing against all of the gold supposedly stored in Ft. Knox? Is gold predicting a crisis that would leave the global money system in wreckage? We’ll have our answer eventually, but it could already be very late in the game for those seeking the bomb-proof safe haven that gold has always offered.