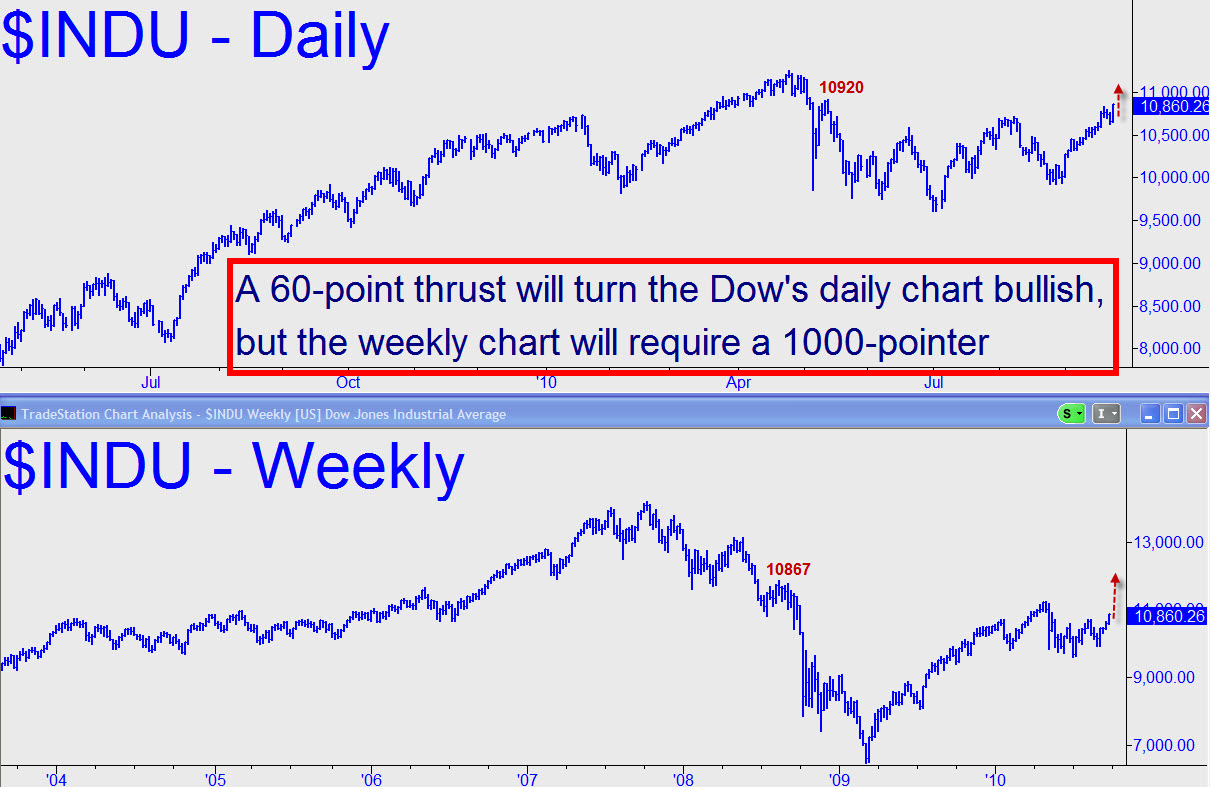

The Mother of All Bear Rallies wafted on Friday to within easy distance of re-igniting a bull trend that had seemed unstoppable until last spring. Back then, buyers who had driven the broad averages higher for fourteen months at an unsustainable, 45-degree pitch went limp, sending stocks into a vexatious roller-coaster ride of thousand-point ups and downs that have defied easy categorization as either consolidation or distribution. However, the bulls will have a chance to take charge unambiguously on Monday when shares begin to trade, since it will take a mere 60-point rally, to 10921, to turn the Dow’s daily chart bullish. We should note, however, that that wouldn’t quite clinch the bullish case for the longer-term, since a thousand-point rally to at least 11868 is needed.

{kind=link}

Last week’s dramatic liftoff was brought on by the usual suspects, including: 1) the virtual absence of sellers in a market that has been driven 99% by computer-trading and institutional prop desks; 2) a sufficient quantity of aggressively spun but ultimately meaningless “good” news to drive short-squeeze buying through key resistance; 3) a helping hand from opportunistic buying of U.S. index-futures in illiquid, overnight markets; and 4) a mood-driven window of opportunity for the mountebanks, self-promoters and insipid droolers of the talking-head world to interpret whatever news hits the tape as bullish. For example, there was the marquee-named Quincy Krosby. She is the chief market strategist at Prudential Financial, and her cue was an item on the tape that said U.S. companies were spending more, according to the Wall Street Journal, “at a time when the global economy looks to be on the rise.” No matter that the rising appearance of things was as fleeting as dew on cactus, or that the supposed uptick in corporate spending apparently involved just a handful of high-tech firms. Such details were easily overlooked in a moment when virtually any and all news that crossed the wire was going to be construed as bullish.

‘Free’ Bear’s Bear

Naturally, this pendulum swing toward giddiness included the obligatory, bullish take on the U.S. dollar’s ongoing collapse — about how this would “help” U.S. exports, even if we hardly export anything any more save Hollywood movies and other cultural flotsam. The resident genius at Jefferies, market analyst Art Hogan, took a pot-shot at all of the supposedly silly talk about a double-dip recession. “The concept of a double-dip recession has been replaced with slow and steady improvement [oh really?], and even if we don’t get it, we have a Federal Reserve that’s ready to step in and support the rally,” said Hogan. Not to be outdone at elevating breathtaking stupidity to the status of cult religion, the Journal itself provided this jaw-dropping transitional paragraph, as though it were 2007 again: “The market also received a boost from the Federal Reserve’s message earlier in the week that it is prepared to take action if the economy weakens.” This sentence pretty much sums up the forces that are driving the markets higher. It’s OPM at work, and who are we to argue with such factually-challenged craziness?

If you’d like to jump on the bullish bandwagon with your eyes wide open, and to keep tabs on a potentially powerful rally through the gimlet eye of a bear’s bear, we’d suggest that you check out our daily trading recommendations via a free trial to Rick’s Picks. Just because the rally is silly, stupid and ultimately leads to the edge of a cliff is no reason why we can’t enjoy and perhaps profit from it.

(If you’d like to have Rick’s Picks commentary delivered free each day to your e-mail box, click here.)

It has been said that the greatest export of the West to China was communism. Marx said that history repeats itself, first as tragedy, second as farce.

In light of Marx’s adage, is the World Expo of 2010, being held in Shanghai, an omen of the future?

China’s first world fair took place in 1910 and in the following year the Manchu dynasty fell.

History suggest to me that in the coming depression, set in motion by rising interest rates to combat inflation, especially from QEII, that the Communist Party will collapse and that China will descend into anarchy/civil war leading to balkanization – a fate that will also befall America.

“…there was another reason for [Japan] attacking China, which went to the roots of the Japanese dynamic impulse. ‘They are peculiarly sensitive’, wrote Kurt Singer, ‘to the smell of decay, however well screened; and they will strike at the enemy whose core appears to betray a lack of firmness …. Their readiness, in the face of apparent odds, to attack wherever they can smell decomposition makes them appear as true successors of the Huns, Avars, Mongols and other “scourges of God”.’ This shark like instincts to savage the stricken had been proved sound in their assault upon Tsarist Russia. It was to be the source of their extraordinary gamble for Asian and Pacific paramountcy in 1941. Now, in the 1920s, it was to lead them irresistibly to China, where the stench of social and national gangrene was unmistakable” (Paul Johnson, Modern Times, (London: Orion Books, 1994), p.190).

China may yet regret ‘shaming’ Japan, over the arrest of the Chinese fishing boat captain.

History suggest that there will be a revival of military shintoism in Japan in response to the next Great Depression.

“Rereading history books and the testimony of those who experienced the transition from the Taisho democracy of the 1920s to the militarism of the 1930s, I marvel at how quickly a society with give-and-take politics, a strong labour movement, active and contentious writers and intellectuals, and an urban populace with a jazzy pop culture could be transformed into a nation in armour” (Frank Gibney, Reinventing Japan…Again, Foreign Policy, Summer 2000, p.80).

I would not be surprised by a Japanese coalition attacking China at the same time that they amount an invasion of Australia and New Zealand, as a European, Russian and South American alliance takes out America.