Fake Videos Are an Insidious Evil

Although we used to feature edgy market commentaries in this space, the time and effort spent crafting them is now devoted to making the Rick’s Picks Trading Room an unbeatable source of timely ideas for novices and professionals. I must also tell you that your editor was deeply tired of having to write regularly about a stock market energized by clueless money managers whose only trick is recklessly throwing Other People’s Money at some moronic investment-theme-of-the-week. You should still check here weekly, since I will continue to post links to my latest interviews and to offer visual enticements designed to entertain, enlighten and even warn you. Much of it will come from YouTube, since their video catalog is endlessly fascinating and vast. Submissions, including home videos, are welcome and should be sent to this address. To view this week’s offering, click here and watch the fake T&A hottie complete her fake dive. It is yet one more piece of AI-generated, click-bait garbage that is slowly eroding our trust in photo and video images. The trend is unstoppable, since even a teenager with help from Grok or Claude could have produced the ginned-up video you see. But we can at least learn how to spot the fakes, and you need only read the comments section associated with the hottie’s fictional dive to sharpen your eye for visual flimflammery. For starters, notice how her feet are not properly oriented to the platform. There are innumerable other flaws in this video to be found and mentally catalogued. Magritte’s famous painting, “Ceci n’est pas un pipe” may have foreshadowed far more than the artist ever imagined.

{kind=link}

Subscribe Free!

The analytical ‘touts’ below, overhauled each Sunday and updated 24/7, will continue as always, as will their barbed emphasis on the similarities between Wall Street and sleazy carnival midways. The remarkable accuracy of our trend calls and price targets is a matter of daily record and must be observed up-close to be believed. Sign up for a free trial with access to all site amenities by clicking here (no credit card needed). Then click here for my most recent interview with Howe Street’s This Week in Money. We talk about the AI boom in a way that will enable you to understand why a bust is inevitable. It comes down to weighing the countless trillions of dollars that are being invested against expected revenues. How much are you currently paying for Claude/Grok/Chat GPT? How much more would you pay if their respective developers try to put the squeeze on you to recoup their costs? That’s my point, and it applies not only to individual customers, but equally to large corporate customers as well. Greed and hubris have blinded AI’s purveyors to its very finite limitations as a product we will pay for. Given the sums involved, this holds dire implications for the stock market and the economy. There is no turning back for investors, only down.

$TNX.X – 10-Year Note Rate (Last:4.66%)

One might think manipulating yields on the Ten-Year Note would be beyond the reach, even, of Donald Trump and those who serve him in the shadowy corridors of financial power. And yet, each time the interest rate moves in earnest toward the psychologically hazardous 5% level, it swiftly retreats as

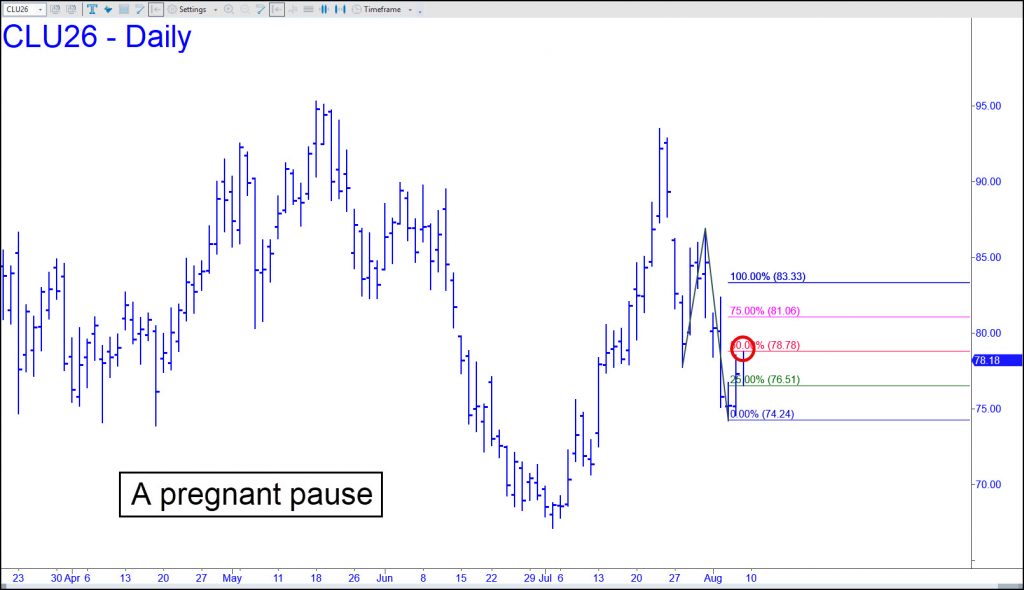

CLU26 – September Crude (Last:78.18)

Friday’s muted rally stalled just a penny from the 78.78 midpoint Hidden Pivot resistance shown in the chart. This could hardly have surprised, since none of the wack-os who trade crude could conceivably know what kind of fake rabbit Trump will pull out of his hat over the weekend. By

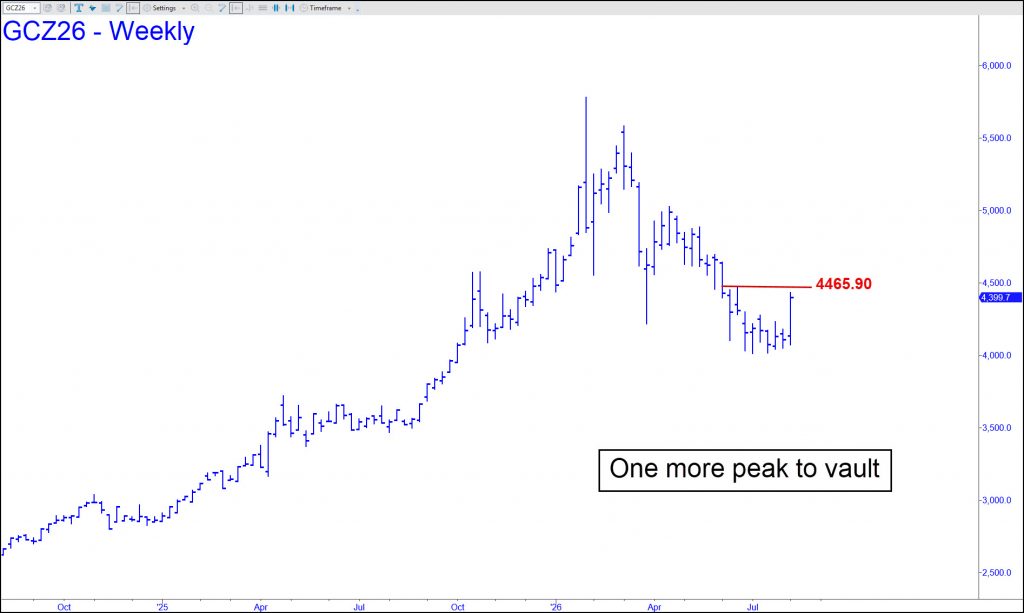

$GCZ26 – December Gold (Last:4399.70)

Did gold’s bear market end with the 4016 low recorded a month ago? We’ll likely have a definitive answer next week if the powerful upthrust of the last two days continues, exceeding the 4465.90 peak shown. That would mean the futures had exceeded two ‘external’ peaks on the weekly chart

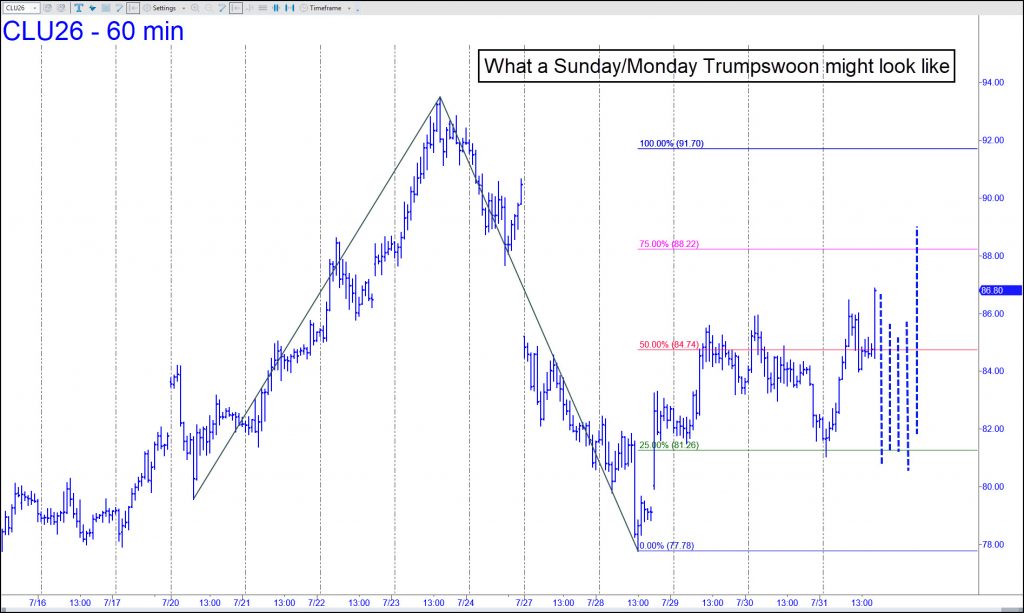

CLU26 – September Crude (Last:86.80)

Trading in NYMEX Crude won’t start for another hour, so I’ve had to imagine a pattern to predict how things might turn out. It is a foregone conclusion that quotes will open significantly lower, since Trump, as fully expected, has announced on a Sunday yet another ceasefire. This dog-and-pony show